Archive for June 2013

SERIES: Investing Fundamentals Part 4 – Unleash the Power of Compound Interest

Welcome to the latest series at JosephSangl.com – “Investing Fundamentals” Investing is consistently rated by our audience as one of the most confusing topics they face. In this series, we are going to share some foundational principles that can really help you understand investing better!

Four Unleash the power of compound interest

Compound interest is the payment of money to you from companies you have allowed to use your money.

For example let’s say we have $100 in an investment account that grew to $105 in one year. This is the equivalent of 5% interest.

Now suppose the $105 is left alone for another year and continues to grow at a rate of 5%. Will it be paid another $5 interest when the second year is up? No! It will be paid $5.25 because interest was received on $105 – not just $100. In other words, the interest money also earns interest! This is why you hear people say, “My money is working for me.”

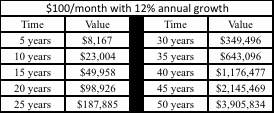

Take a look at the below example of a $100/month investment growing at an annual compounded rate of 12%.

Remember you are only investing $100 each month! Even though after 40 years you will have only invested $48,000 of your own money, your account balance will be $1,176,477! This means that $1,128,477 is the interest you have gained!

Now do you see the POWER of compound interest?

Where do you find investments that offer 12% return? I have found no investments that return 12% every single year, but I have found several mutual funds that average over 12% return over the past 50 years. Some years could lose 15% while others could gain 30%. You can see a list of my current investments HERE.

How to maximize your investment growth:

- Invest enough to receive the entire company match. By investing in an employer-sponsored retirement plan that matches some of your contributions, you could even receive a 50% or 100% return!

- Monitor your investments at least every six months. I track my investments at the end of every single month. This helps me understand how each one is performing and allows me to make necessary adjustments.

- Consider investments beyond the stock market. The stock market is just one place to invest. Consider small businesses, real estate, and intellectual property – like patents and licensing rights. Remember a higher interest rate almost always means a higher risk.

STEP TO TAKE:

- Establish a consistent investing habit. Invest every single paycheck into your retirement account for the rest of your working life. Even if you can only invest a small amount, it will add up to more than you can imagine!

RECOMMENDED RESOURCE:

- OXEN – The KEY to an Abundant Harvest In this book, Joe shares the steps you can take to maximize your money through investing!

- This book is also available via Amazon and Kindle.

NOTE: This post contributed by IWBNIN intern – Craig Fatt

SERIES: Investing Fundamentals Part 3 – Get the Free Money

Welcome to the latest series at JosephSangl.com – “Investing Fundamentals” Investing is consistently rated by our audience as one of the most confusing topics they face. In this series, we are going to share some foundational principles that can really help you understand investing better!

Three Get the Free Money

Yes, I said FREE money. Many employers will match a portion of your contributions into a self-directed retirement plan! I encourage you to go to your employer’s human resources department and sign up for the retirement plan. Start investing money into it immediately! Contribute enough money to obtain the entire employer match. Remember this is really just FREE money!

The company you work for will usually match you up to a certain percent of your pay. I worked for an employer that matched me dollar-for-dollar up to 8% of my pay (100% automatic rate of return!!!). Another matched dollar-for-dollar up to 6% of my pay. Still another matched dollar-for-dollar up to 3% of my pay. Whatever your employer is willing to give you is FREE MONEY!

It is baffling that many people don’t take advantage of these free money opportunities. I have heard several excuses about why people choose not to, excuses like:

- “I can’t afford to contribute.”

- “I’m living paycheck to paycheck already.”

These people are basically saying they can’t afford to be given free money. Doesn’t make a whole lot of sense, huh? This is an opportunity to receive a 100% return on your investment! DO NOT WASTE THIS CHANCE!

STEPS TO TAKE:

- Talk to your employer TODAY and sign up for your company’s retirement plan. Start contributing something – at least enough to get the full match.

- As quickly as possible, increase your investing contribution to at least 10% of your gross income. I know this is a lot of money, but you will NEVER regret this decision.

RECOMMENDED RESOURCE:

- OXEN – The KEY to an Abundant Harvest In this book, Joe shares the steps you can take to maximize your money through investing!

- This book is also available via Amazon and Kindle.

NOTE: This post contributed by IWBNIN intern – Craig Fatt

SERIES: Investing Fundamentals Part 2 – Automate Your Investments

Welcome to the latest series at JosephSangl.com – “Investing Fundamentals” Investing is consistently rated by our audience as one of the most confusing topics they face. In this series, we are going to share some foundational principles that can really help you understand investing better!

Two Automate Your Investments

Make your investments automatic! You can set up your bank account to auto-draft money into different accounts like a 401k or a child’s 529 college-savings plan. This will prevent you from forgetting or trying to use the money elsewhere because you will never even notice it’s gone!

If you ever have to switch between banks then the auto-drafting will stop so you will need to get it set up at your new bank. I know from firsthand experience how hard it can be to write a check to my savings account and my daughter’s 529 college-savings plan. There are moments where you will think “Wow! I could really use this money elsewhere!”

If I had to write a check every month to my savings account or to my investment accounts, there is a high likelihood my investing plan would be seriously off-track. MAKE IT AUTOMATIC!

By making your investments automatic you will see your net worth increase every single month. Making investments automatic eliminates the possibility of using this money for splurge purchases. This is awesome for those of us who are highly susceptible to spend any and all extra money!

STEPS TO TAKE:

- Go to your bank and tell them you want to start auto-drafting money into an investment account such as a 401(k) or any retirement account or also a 529 college-savings plan. I also do this with my savings account!

RECOMMENDED RESOURCE:

- OXEN – The KEY to an Abundant Harvest In this book, Joe shares the steps you can take to maximize your money through investing!

- This book is also available via Amazon and Kindle.

NOTE: This post contributed by IWBNIN intern – Craig Fatt

SERIES: Investing Fundamentals Part 1 – Diversify Yourself

Welcome to the latest series at JosephSangl.com – “Investing Fundamentals” Investing is consistently rated by our audience as one of the most confusing topics they face. In this series, we are going to share some foundational principles that can really help you understand investing better!

One Diversify Yourself

I’m sure you have heard someone say don’t put all your eggs in one basket. That directly relates to investing! A key step when investing is to diversify your investments. For example you should not put all the money you can into one company’s stock, instead spread your investment out. By spreading out your investment you greatly lower the risk of your investment.

You can research countless times where people have put a large portion of their money into one company only to have it fail, which means that they lost A LOT of money. Several people lost large sums of money when they only invested in Enron during the early 2000’s and then it went under. If these people would have diversified their investments they could have softened the blow.

An easy way for you to diversify your investments is to look into investing in mutual funds. A mutual fund allows you to purchase a portion of many stocks and bonds with the single share purchase so you are automatically diversified even though you have only bought 1 share! Also DON’T JUST THINK ABOUT STOCKS. Invest in a new business or a home that can be rented out. You don’t have to just think about the stock market when it comes to investments! You have a world of things to invest in! Real estate, land, new businesses, or even your own business.

STEPS TO TAKE:

- Review your investment choices. Are they diverse?

- Are you only investing in one type of company? If yes, take steps to address right away!

- What other investments could you make outside of the stock market?

RECOMMENDED RESOURCE:

- OXEN – The KEY to an Abundant Harvest In this book, Joe shares the steps you can take to maximize your money through investing!

- This book is also available via Amazon and Kindle.

NOTE: This post contributed by IWBNIN intern – Craig Fatt

Saving For Known Upcoming Non-Monthly Expenses

Everyone must save for three things: (1) Emergencies, (2) Known Upcoming Non-Monthly Expenses, and (3) Dreams

Of these three, it seems like saving for #2 – Known Upcoming Non-Monthly Expenses is the most difficult and creates the most issues with budgeting.

Here’s why Known Upcoming Non-Monthly Expenses create severe budgeting difficulty:

- They are non-monthly Because of this, we tend to forget about them until they show up

- They are usually larger expenses Property taxes, insurance premiums, Christmas, vacation, car maintenance and repairs, and insurance deductibles usually have larger price tags than typical monthly expenses

- We don’t save for the expenses monthly We wait until the bill arrives and then we are forced to scramble in an attempt to pay for it

This is why I call these type of expenses “Budget Crushing Expenses.” You can avoid this stress entirely by creating a Known Upcoming Expenses saving plan!

Here’s a step-by-step way for you to eliminate “Budget Crushing Expenses” from your life:

- Download our free “Known Upcoming Expenses Calculator” tool HERE.

- Enter all your “Known Upcoming Expenses” into the tool – include the annual expense of each line item.

- Enter your “# of Pay Periods Per Year” into the tool – enter “12” if paid monthly, “26” if paid every 2 weeks, “52” if paid weekly, and “24” if paid twice each month.

- You have now calculated the amount you need to save out of each paycheck to ensure all of your Known Upcoming Non-Monthly Expenses are covered.

- BONUS STEP: Set up an on-line savings account (I use Capital One 360 – formerly known as ING Direct) and make your savings automatic. In other words, you can set up automated transfers to your on-line savings account. This allows you to “set it and forget it” and KNOW you’re major known upcoming non-monthly expenses are covered!

AUTHOR’S NOTE: I am paid monthly. I have set up a monthly transfer to happen on the 6th day of the month from my regular bill-paying bank account to my Capital One 360 account. It may not be the most exciting thing in life, but it is INCREDIBLE to know I have eliminated “budget crushing expenses” from my life!