Archive for July 2006

Home mortgage interest deduction a good idea?

Absolutely! If you have a mortgage and are paying interest, it is very important to take the mortgage interest deduction.

One thing I have heard commonly stated is the statement that “I do not pay off my mortgage early because I do not want to lose the mortgage interest deduction.” I believe this saying was initiated by banks 🙂 Here is why. Look at the example below.

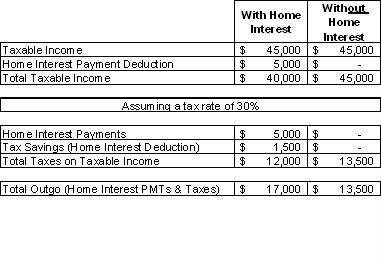

The Mortgage Interest Deduction

Let’s say you paid $5,000 in interest on your mortgage last year. By taking the deduction, you effectively reduce your taxable income by $5,000. You receive back the tax rate on that home mortgage interest deduction. If your tax rate is 30%, you get back $1,500 (30% of $5,000). The bank gets to keep the $5,000 you paid in interest. Uncle Sam gets 30% of your taxable income which is now $40,000 because you were able to reduce your taxable income by the interest you paid. The total net OUTGO from you to Uncle Sam and the bank is $17,000!

The Paid-Off House Scenario

Well, you are living life pretty good in your debt-free condition! So, now you no longer pay interest to the bank (sorry!). This means that you will be taxed on the full $45,000. If your tax rate is 30%, the total net OUTGO from you to Uncle Sam is $13,500!

$3,500 LESS OUTGO from you to someone else.

So that is why I believe that the banks started the statement, “I do not pay off my mortgage early because I do not want to lose the mortgage interest deduction.” If you do pay off your mortgage, the banks will not get any of your money!

THINK and you will prosper!

Save at the dentist …

A lady who went through the personal finance course that I coordinate told me of her trip to the dentist.

The dentist told her that she needed a crown. The cost of the crown was to be $650. She told the dentist, “I am paying cash. $250!” The surprised dentist responded, “$325.”

What a deal!

What a thought! You see, the dentist is performing a service. A service is negotiable. When you are paying cash out of your own pocket, you are more apt to question the fee.

It makes one stop and think about the impact of 100% payment insurance. It doesn’t make the patient pay out of their own pocket, so they are less apt to question the fee.

Go out and ask for a better deal!

How to pay for your next car.

In conversation with a friend recently, he mentioned that he is starting to check out the new cars because he is going to be buying a car in three years. He has owned his current vehicle for seven years. His goal is to keep it for ten years. NOTE: This is how you win financially. Buying depreciating assets sparingly. Do not buy a new car every single year.

Anyway, I asked him if he was planning on paying cash for it. The answer was an uncertain, “No.” It was almost quizzical. It was like, “Who pays cash for a new car?” or maybe “How would I pay cash for a new car?”

Here’s how! YOU HAVE THREE YEARS!!!

Take the expected purchase price of the vehicle in three years. Let’s say that it will be a $20,000 vehicle. You have 36 months until you will be purchasing the vehicle. Divide the $20,000 by 36. You need to save $555.56/month in order to have $20,000 in cash three years from now.

IT IS THAT SIMPLE!!!

You may be saying, “Joe, there is NO WAY I can save $555.56/month for each of the next 36 months!” My answer? THEN YOU CANNOT AFFORD A $20,000 CAR IN 36 MONTHS!!! I bet you will get a raise between now and then. I bet you will get a tax refund between now and then. I sincerely hope that you will be paying off your consumer debt between now and then.

Listen – If you really want the $20,000 car in 36 months, save $555.56/month. We don’t do debt around here.

IT IS THAT SIMPLE!