Archive for July 2009

How Much Money Do You Need To Retire Well

Do you know how much money you will need to retire well (independent of Social Security)?

There are many ways to calculate an estimate, but I really like the Retirement Nest-Egg Required calculator that we have placed in the FREE TOOLS section.

To calculate your number, you will need to know two numbers:

- The annual amount you want to live on at retirement (in today’s dollars)

- The number of years until you retire

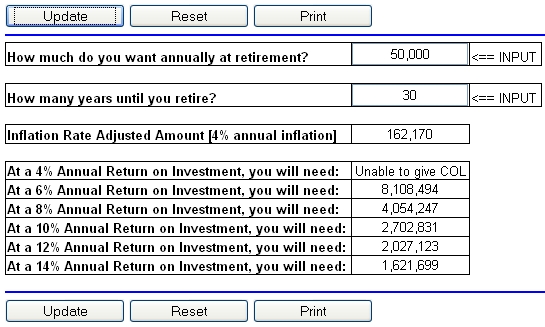

Suppose one wants $50,000/year (today’s dollars) during retirement and plans to retire in thirty years. Punch the numbers into the Retirement Nest-Egg Required calculator and this is what you will see:

Because inflation erodes the spending power of money, the annual amount we want must be adjusted. Using an assumed inflation rate of 4%, one will need $162,170/year in thirty years to have the same spending power of $50,000 today.

At different rates of return, you can see different amounts that need to be saved. Eight percent is a common rate of return on investment that financial planners use.

What is your number? Are you going to achieve it?

SERIES: Save Money On Groceries – Aldi

Welcome to the latest series from the I Was Broke. Now I'm Not. Team – Save Money On Groceries

Ready to save $100 – $200 every month on groceries? Read this series, and we will show you how!

Aldi Grocery Store

Aldi is the cheapest grocery store I have ever found. It is first-quality, top-notch food, and I LOVE shopping at this store! It is about 10% – 33% cheaper than the next cheapest grocery store.

I buy cereal, milk, bagels, bread, eggs, cheese, fruit, vegetables, meat, canned foods, and many other products at this store, and I have been very satisfied!

I can only hope that Aldi has a store near you. You can click HERE to see if they do.

Do you shop at Aldi? If so, share your stories!

SERIES: Save Money On Groceries – SouthernSavers.com

Welcome to the latest series from the I Was Broke. Now I'm Not. Team – Save Money On Groceries

Ready to save $100 – $200 every month on groceries? Read this series, and we will show you how!

SouthernSavers.com

Add this website to the ones you check every single day. This website is written by a stay-at-home mom so you KNOW that she will share some incredible deals!

You will find INCREDIBLE deals for at least eleven grocery stores, coupons, and saving tips.

All of the members of the I Was Broke. Now I'm Not. team are crazy about this site.

You can check it out HERE (you should go ahead and SUBSCRIBE).

Have you used Southern Savers? Share your story!

SERIES: Save Money On Groceries – TheGroceryGame.com

Welcome to the latest series from the I Was Broke. Now I’m Not. Team – Save Money On Groceries

Ready to save $100 – $200 every month on groceries? Read this series, and we will show you how!

TheGroceryGame.com

TheGroceryGame.com is very similar to Couponmom.com in the way it lists the best deals matched with coupons to give you unbelievably low costs on groceries. However, the sight is not free. It costs $10 for each two month period for the first grocery store and $5 for each additional grocery store. The advantage to this site is that it has a much larger database of available stores. So if your local grocer is not on the Coupon Mom list you will probably find it here. The site does pay for itself many times over and is worth the money if you cannot get the stores you need from CouponMom.com.

You can sign up for The Grocery Game HERE.

Have you used The Grocery Game? Share your stories!

SERIES: Save Money On Groceries – CouponMom.com

Welcome to the latest series from the I Was Broke. Now I’m Not. Team – Save Money On Groceries

Ready to save $100 – $200 every month on groceries? Read this series, and we will show you how!

CouponMom.com

If you are not using CouponMom.com, there is a high chance that you are way overpaying for your groceries.

In our Financial Learning Experience events, I have the opportunity to share some money saving ideas. Of course, I always wish I had ten or eleven hours to share as many of them as possible, but there is not enough time.

One that I ALWAYS mention however, is CouponMom.com.

Here is how it works:

- Obtain Sunday newspaper coupon booklets (issued by SmartSource, RedPlum, and P&G)

- Mark the date issued on the coupon booklets – do NOT cut the coupons

- Sign up to CouponMom.com (click HERE to sign up – it is FREE!)

- Every week, go to CouponMom.com and pull up your store’s deals under the “Grocery Deals By State”

- CouponMom.com will tell you which coupon booklets to cut coupons from and how to use them to obtain an average of 50% to 85% OFF!

It sounds too good to be true, but I use this myself! I KNOW it to be true! For example, this week I went to Publix (grocery store near my house) and had a bill of $69.00. I received $33.98 OFF after using my coupons. This was not for useless junk that I will never use. This is for cereal, pickles, ice cream, vitamins, toilet paper, paper towels, and many other products that I would purchase anyway.

Have you used this service? If so, share your victory stories! If not, get started and save a ton of money.