Posts by Joseph Sangl

Financial Stress

Do you know what it is like to experience financial stress?

Financial stress impacts family relationships – marriages, parents with children, children with parents, siblings. Financial stress impacts friendships and business partnerships. It can forever destroy your relationship with your spouse.

Why is this?

The way you manage your finances tells a story. It tells a story about what you value, about what is important to you, and about who is important to you. It can also tell a story about what you do not value, about what is unimportant to you, and about who is unimportant to you.

If you spend a majority of your money paying bills for debts (car, house, TV, credit cards, student loans, furniture, boat, lawn mower, etc.) you have signed up for, then it tells a story that having stuff might be more important than saving for retirement.

If you spend everything you make and live from paycheck to paycheck, it could indicate that you do not value security more than you value not having to take time developing a spending plan.

If you give away a pile of money to worthy causes, have taken the time to develop a spending plan that works, are saving for retirement, college, and other notable expenses, and are regularly reviewing your spending habits ON PURPOSE to understand opportunities for better management of your money … it tells me that you are weird and value others and your future more than you value stuff.

Go look at your spending. Does it line up with your values?

By the way, “you” can insert “me” or “I” everywhere “I” have listed “you” and “your” in this diatribe. 🙂

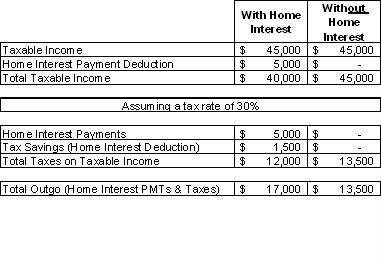

Home mortgage interest deduction a good idea?

Absolutely! If you have a mortgage and are paying interest, it is very important to take the mortgage interest deduction.

One thing I have heard commonly stated is the statement that “I do not pay off my mortgage early because I do not want to lose the mortgage interest deduction.” I believe this saying was initiated by banks 🙂 Here is why. Look at the example below.

The Mortgage Interest Deduction

Let’s say you paid $5,000 in interest on your mortgage last year. By taking the deduction, you effectively reduce your taxable income by $5,000. You receive back the tax rate on that home mortgage interest deduction. If your tax rate is 30%, you get back $1,500 (30% of $5,000). The bank gets to keep the $5,000 you paid in interest. Uncle Sam gets 30% of your taxable income which is now $40,000 because you were able to reduce your taxable income by the interest you paid. The total net OUTGO from you to Uncle Sam and the bank is $17,000!

The Paid-Off House Scenario

Well, you are living life pretty good in your debt-free condition! So, now you no longer pay interest to the bank (sorry!). This means that you will be taxed on the full $45,000. If your tax rate is 30%, the total net OUTGO from you to Uncle Sam is $13,500!

$3,500 LESS OUTGO from you to someone else.

So that is why I believe that the banks started the statement, “I do not pay off my mortgage early because I do not want to lose the mortgage interest deduction.” If you do pay off your mortgage, the banks will not get any of your money!

THINK and you will prosper!

Save at the dentist …

A lady who went through the personal finance course that I coordinate told me of her trip to the dentist.

The dentist told her that she needed a crown. The cost of the crown was to be $650. She told the dentist, “I am paying cash. $250!” The surprised dentist responded, “$325.”

What a deal!

What a thought! You see, the dentist is performing a service. A service is negotiable. When you are paying cash out of your own pocket, you are more apt to question the fee.

It makes one stop and think about the impact of 100% payment insurance. It doesn’t make the patient pay out of their own pocket, so they are less apt to question the fee.

Go out and ask for a better deal!

How to pay for your next car.

In conversation with a friend recently, he mentioned that he is starting to check out the new cars because he is going to be buying a car in three years. He has owned his current vehicle for seven years. His goal is to keep it for ten years. NOTE: This is how you win financially. Buying depreciating assets sparingly. Do not buy a new car every single year.

Anyway, I asked him if he was planning on paying cash for it. The answer was an uncertain, “No.” It was almost quizzical. It was like, “Who pays cash for a new car?” or maybe “How would I pay cash for a new car?”

Here’s how! YOU HAVE THREE YEARS!!!

Take the expected purchase price of the vehicle in three years. Let’s say that it will be a $20,000 vehicle. You have 36 months until you will be purchasing the vehicle. Divide the $20,000 by 36. You need to save $555.56/month in order to have $20,000 in cash three years from now.

IT IS THAT SIMPLE!!!

You may be saying, “Joe, there is NO WAY I can save $555.56/month for each of the next 36 months!” My answer? THEN YOU CANNOT AFFORD A $20,000 CAR IN 36 MONTHS!!! I bet you will get a raise between now and then. I bet you will get a tax refund between now and then. I sincerely hope that you will be paying off your consumer debt between now and then.

Listen – If you really want the $20,000 car in 36 months, save $555.56/month. We don’t do debt around here.

IT IS THAT SIMPLE!

Stop living from paycheck to paycheck!

A recent study from ACNielsen revealed that about 1 in 4 Americans say that they do not have any spare cash. No wiggle room. No room for an error. No room for an emergency. No room for life to happen.

Question: That new car – is it worth being broke over?

Question: That student loan – is it worth the degree you will receive?

Question: That furniture – is it really so important that you could not save up and pay cash for it?

Question: What would you be able to do if you had cash available to you?

I just completed reading the story in ESPN The Magazine (June 19, 2006 edition) about PGA Tour Pro John Daly. He states that when he showed up to St. Andrews for the British Open Major Championship in 1995, he was in debt almost $4,000,000. He states, “The only way I’d been able to keep my head above water was to turn all my quarterly endorsement income over to the casinos (his debtors), and then run myself ragged by playing all over the world for appearance fees and doing too many corporate outings, all because I needed the money to feed the beast. The British Open saved me. Not because of the winner’s purse – it was only … $200,000 back then. But when you throw in the bonuses from all my sponsors, I took at $1 million-plus haul away from the Old Course. All that went to the casinos.”

Paycheck to paycheck even when making millions. It is a VERY SIMPLE math equation.

INCOME – OUTGO = EXACTLY ZERO

OUTGO needs to include savings for emergencies and otherwise unexpected financial needs. If not, you will continue to live paycheck to paycheck.

Living paycheck to paycheck robs you of your ability to dream. It shoots down hope. It leads to depression and despair. It can lead to a feeling of inadequacy. It will force you to turn to debt when any small issue arises. It drives a wedge between husband and wife – between parents and children. It leads to increased stress and high blood pressure. It prevents people from following their dreams. It paralyzes you.

You may think I am overstating this, but I don’t think so. I have seen it with my own eyes. I have stared hopeless persons in the eye. I have heard the despair in their voices. I used to live paycheck to paycheck and was in debt up to my eyeballs. No more. There is no house, no furniture, no car, no vacation, no investment scheme, no student loan, no … NOT ANYTHING that can ever get me to live paycheck to paycheck again. Life is just way too short to spend all of my time worrying about how I will pay this month’s bills.

Make a commitment to change NOW!

Need help? Contact me.