Posts by jsangl

Marching To Debt Freedom – Couple #1 – Month 13

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now over a year into their Debt Freedom March.

Couple #1's Thoughts This Month

I am so thankful for your help and encouragement in these tough times. If we were carrying our previous levels of debt it would be stressful to say the least. We are seeing our 401k shrivel but we all know that will return with time and stability. I only hope Americans now see that being in debt is dangerous combination of timing and chance.

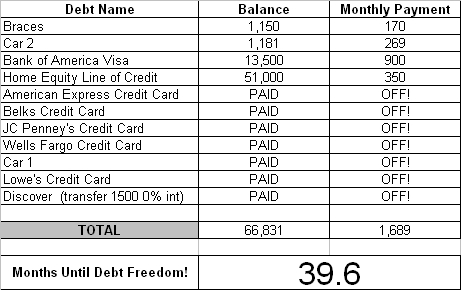

Updated Debt Freedom Date

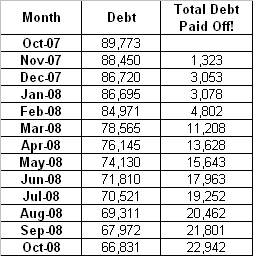

Month By Month Progress

Sangl Says …

Another boring month of debt reduction … 🙂 Couple #1 has figured this thing out. They have a plan that is working, and that means more debt has left. Way to go!

Readers …

How is your Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction HERE.

Receive each post automatically in your E-MAIL by clicking HERE.

NEXT STEPS – A New Part Of The Crusade – Part 1

Before this moment, there were four key ways this crusade was carried out:

- Speaking (Churches, Businesses, and Civic Organizations – Upcoming Events HERE)

- Teaching (Financial Learning Experience, Financial Freedom Experience)

- One-On-One Financial Counseling (Financial Counseling Experience)

- Resources (I Was Broke. Now I'm Not. and its Group Study)

Today, I am PUMPED to introduce a fifth way that this crusade is carried out: NEXT STEPS

Let me tell you how this newest part of the crusade came about.

First I will start by reiterating my passion. It is my passion to see others accomplish far more than they ever thought possible with their personal finances. The reason I am so passionate about this is because I believe that when people are financially free, they are much more likely to go do EXACTLY what they have been put on this earth to do.

As I partner with churches and businesses throughout the nation to help teach PRACTICAL personal finance tools, my passion and this vision drives me to constantly ask the question, "What is a PRACTICAL next step that we can offer folks?"

Let me be more specific.

- "After this message series on money, what is the PRACTICAL next step we can offer to help people take their finances to the next level?"

- "After Joe speaks at our business, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

- "After the Financial Learning Experience or Financial Freedom Experience, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

- "After someone reads I Was Broke. Now I'm Not., what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

- "After someone participates in the I Was Broke. Now I'm Not. Group Study, what is a PRACTICAL next step we can offer to help people take their finances to the next level?"

Next Steps is a website created to answer these questions. Over the next several weeks, there will be several series written about the practical tools and solutions that we have placed on the site. I encourage you to check it out, and see if there are ways that can help you achieve YOUR next steps!

PrintPlace.com

Book Review: The Five Dysfunctions Of A Team

I have recently finished reading The Five Dysfunctions Of A Team written by Patrick Lencioni.

I have recently finished reading The Five Dysfunctions Of A Team written by Patrick Lencioni.

A GREAT book. If you are a leader, this book will cause you to think through your team in a new way and could quite possibly take your team to a new level of performance.

Here are some key points I took from this book:

- Everything we do should be about making the company succeed

- No matter how good an individual team member is, everyone loses if the team loses

- Fear of Conflict = Artificial harmony

- Boring Meetings = Unnecessary Meetings

- It is important for a leadership team to keep walls between their teams torn down. Teams naturally tend to move toward isolation and a "Those guys over there are terrible, but we have got our act together" mentality.

Well written. I read this book in five to ten minute sections, and I found that it was very effective for me to read it this way. It allowed me to process what I read and then come back to it later having thought it through.

SERIES: Sell Car With Negative Equity – Part 5

Welcome to the latest series – "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Part 1 – Recognize How Much A Car Really Costs

Part 2 – Determine Your Car's Negative Equity

Part 3 – Sell The Car With Negative Equity – Option A – Pay Off The Balance

Part 4 – Sell The Car With Negative Equity – Option B – Transfer The Negative Equity Balance

Part 5 – Benefits Of Selling A Car With Negative Equity

Lower Debt!

This is obvious, but it is a wonderful benefit of eliminating the car with negative equity. In the example used in this series, debt has been reduced by $18,000 in Option A or $12,000 in Option B. Either one is fantastic!

Money Freed Up Every Month!

This is also obvious, but the monthly payment will be eliminated or vastly reduced. This allows one to have more margin in their monthly finances to give, save, or invest (three of my favorite parts of money!).

Not so obvious is the reduction in other fringe expenses. Car insurance will go down. Car property taxes will go down. Gasoline consumption will go down. Car repair costs will go down. These can total up to hundreds of dollars in savings each month!

Margin

When all of the money leaves as soon as it is earned and one is living paycheck-to-paycheck with zero margin for life to happen, it creates serious stress. By eliminating debt and its related payments, one gains tons of financial freedom and drops loads of stress.

Final Note: I know that this stuff is HARD, but I am convinced that financial freedom is worth all of the effort that it takes. When Jenn and I embarked on our debt freedom march, it seemed like it would take forever. Fourteen months later, we were debt free. That was in February 2004. We have never looked back. No car, TV, boat, lawn mower, or Llama has looked good enough for payments. Frankly, a new house does not even look good enough for house payments. We have worked way too hard to achieve financial freedom to fall back into the debt trap. It has been SO WORTH IT! You can read more of my family's story HERE.