Posts by jsangl

Choosing Mutual Funds – Part 3

Welcome to the latest series on JosephSangl.com – "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One What is a mutual fund?

Part Two Establish investment goals

Part Three Types of mutual funds

There are literally THOUSANDS of mutual funds available in the marketplace today. Each mutual fund is usually assigned to a particular family of mutual funds.

Here are some common categories of mutual funds …

- International Stock Fund

- Aggressive Growth Stock Fund

- Growth Stock Fund

- Growth & Income Stock Fund

- Equity-Income Fund

- Balanced Fund

- Bond Fund

- Value Fund

- Industry-Specific Funds (like Healthcare Fund or Pharmaceutical Fund)

- Index Funds (S&P 500, Russell 2000, etc.)

If you purchase ownership in an International Stock Mutual Fund, you can bet that it is primarily investing in international companies. If it is an Aggressive Growth Stock Mutual Fund, you would expect to see the mutual fund purchasing shares of companies that are growing like crazy.

Each family of funds has a general "feel" to it. The International and Aggressive Growth Stock Mutual Funds tend to have wild swings in performance. One year it could grow 40% and the next it could lose 25%. It feels like you are on a great roller coaster ride at Six Flags!

Growth & Income, Equity-Income, and Balanced Funds are more stable and predictable.

Index Funds track specific market indexes like the S&P 500 and the Russell 2000.

In the next post, I will be sharing how to find mutual funds that meet your investment goals.

Automatically receive each post in your E-MAIL

My first book, "I Was Broke. Now I'm Not.", was released on January 20th. It is available via PAYPAL or AMAZON or BORDERS.

Choosing Mutual Funds – Part 2

Welcome to the latest series on JosephSangl.com – "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

In Part One, I reviewed what a mutual fund is.

Part Two – Establish Investment Goals

My personal investment goals guide my mutual fund choices. First you should know a couple of things about me.

- I view my investments as money that I will not touch for at least five years.

- I prefer mutual funds over individual company stocks. I do own one individual company stock, but I will not allow an individual company stock to exceed 10% of my overall portfolio.

My investment goals are GROWTH, GROWTH, and more GROWTH. I do not need my investments to produce income for me as I am in my early 30s. I want my money to GROW. This means that I invest in mutual funds that are purchasing stock of companies that are experiencing major growth (like Google).

Now, if I were retired, I would want my investments to produce income so I would be searching for mutual funds that invest in companies that are paying dividends to its shareholders (like Wal-Mart, Microsoft).

If I were approaching retirement, I would be moving the money that I would need in the next five years to much more stable and secure investments.

In the next part of this series, I will be reviewing the different types of mutual funds. Knowing one's individual investment goals makes the selection of a mutual fund category much easier.

Automatically receive each post in your E-MAIL

My first book, "I Was Broke. Now I'm Not.", was released on January 20th. It is available via PAYPAL or AMAZON or BORDERS.

Choosing Mutual Funds – Part 1

Welcome to the latest series on JosephSangl.com – "Choosing Mutual Funds"

In this series, I will be sharing how I choose mutual funds. It should be noted that I do not sell investment products nor am I professional in the mutual fund industry. This is my own personal philosophy for choosing mutual funds.

Part One – What is a Mutual Fund?

This is THE number one question that I receive when I am teaching the Financial Learning Experience and Financial Freedom Experiences. Mutual funds can certainly sound confusing – especially when there are so many options available. So for those who do not know what a mutual fund is, let me explain it the best I know how.

If something has been FUNDED, it means that money has been given to it.

If you and I come to a MUTUAL agreement, it means that we both were involved in making the agreement.

So if you and I have MUTUALLY FUNDED a project, then it means that we both provided money for the project.

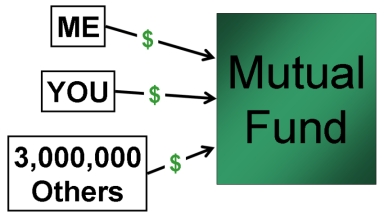

A MUTUAL FUND means that you and I have both put our money in the same place. It is not unusual for a mutual fund to have over 5,000,000 people MUTUALLY FUNDING the same investment.

So we have mutually funded an investment along with three or four million of our closest friends. The amount you have invested is different from how much I have invested, but it is all in the same place. I have drawn a picture to illustrate this. Please marvel at my graphic art skills.

So, we now all understand that we have mutually funded this investment and that it is called a mutual fund. The next question to answer is: "Where does the money go once it is in the mutual fund?"

Well, each mutual fund has a specific objective. Some mutual funds have an objective to produce income. Others have an objective to maximize the long-term growth of the invested money. Still others may have an objective to invest only in international companies. The bottom line is that each mutual fund has a specific objective or charter.

Based upon a mutual fund's charter, the mutual fund managers will purchase part-ownership in a lot of companies. I have employed my terrific graphics skills to illustrate this.

The Mutual Fund managers use the money provided by you, me, and three million of our closest friends to purchase ownership in anywhere from 50 to over 1,000 companies. As these companies earn profits and grow, the value of the investment grows. This means that each individual who owns a portion of the mutual fund can enjoy that growth as well.

So that is what a mutual fund is. I hope that it helped those who may have been confused. In the next part of this series, I will discuss how individual investment goals help guide one's mutual fund selection decisions.

TOOLS: Calculate Mortgage Payment

Welcome to the latest series on the wildly popular website – www.JosephSangl.com! With this series, I will be sharing how you can use some of the calculators from the "TOOLS" page to take your financial plan to the next level.

A mortgage or real estate loan is really the only type of debt that I can tolerate (barely), so here is another FREE tool from the "TOOLS" section of the web site.

To calculate your principal and interest mortgage payment (does NOT include any escrow such as PMI, property taxes, HOA Fees, or hazard insurance), you will need to know three things.

- Interest Rate

- Mortgage Period

- Mortgaged Amount

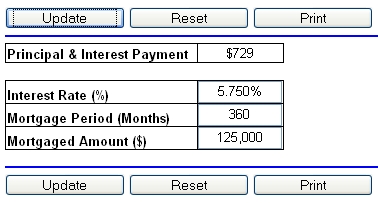

If you want to calculate the monthly principal & interest payment for a fixed-rate 5.750%, thirty-year $125,000 mortgage, pull up the "Mortgage Payment Calculator".

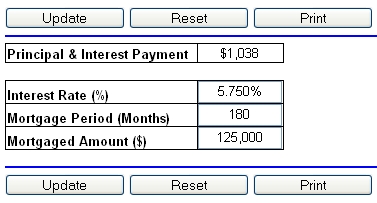

Suppose you want to understand what the P&I payment would be for the same mortgage, but for a 15-year term. Change the mortgage period to 180 months.

The payment goes up $309/month, but one will become debt-free FIFTEEN years sooner!

One could also use this calculator when considering refinancing.

TOOLS: Pay Off The Mortgage Early!

Welcome to the latest series on the wildly popular website – www.JosephSangl.com! With this series, I will be sharing how you can use some of the calculators from the "TOOLS" page to take your financial plan to the next level.

I remember the first day that I put together my "Sangl Family Home Pay-Off Spectacular". I realized just how little of my home I actually owned! When the question was asked of me, "Are you a homeowner?", I could no longer answer, "Yes." Wells Fargo was my homeowner!

With that realization, I decided to pay off my mortgage early. And, God-willing and if the creek doesn't rise, Jenn and I will pay off our house in two years and nine months. How do I know that? Because of another FREE tool on this wildly popular website known as www.JosephSangl.com!

The tool is called the "Early Pay-Off Calculator".

Here is how it works. You need to know three things to use this calculator.

- Mortgage interest rate

- Mortgage balance

- Amount of principal & interest payment that you will be paying (don't include the escrow!)

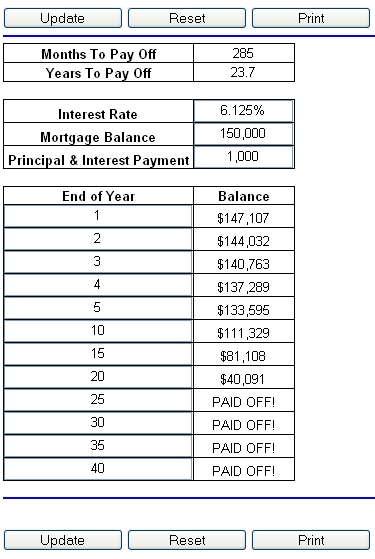

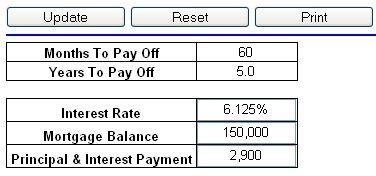

Let's say that one has a thirty-year mortgage with a $150,000 balance and a 6.125% fixed interest rate and a $911/month principal & interest payment.

Suppose you want to know what a monthly principal & interest payment of $1,000 will accomplish. Use the "Early Pay-Off Calculator" to calculate it for you!

Just by paying $89/month extra, the thirty-year mortgage will pay off 6.3 YEARS sooner! How awesome is that?!

One item to note is to designate all extra money to be applied to "principal reduction"! Some of the sly mortgage companies will attempt to apply it to "prepaid interest". That would be a bank error in their favor! Make sure that all extra money is applied to your mortgage principal.

What if the above mortgage holder wanted to pay off their mortgage in five years? You can use the calculator to find out how much would need to be sent each month.

For the low-low price of $2,900 each month, the mortgage will leave in just FIVE years! Can you do that?

Let me ask you another question, if you were debt-free except for the house, could you do this? It is amazing what you can accomplish when you are not bound up in debt!

How early will you pay off your mortgage?

Oh, by the way, you can use this calculate to calculate the early pay-off of ANY type of loan!

In the next part of this series, I will be sharing how you can calculate your mortgage payment.