Posts by jsangl

Favorite Money Quotes

Here are a few of my favorite quotes about money:

- “Live like no one else so later you can live like no one else.” – Dave Ramsey

- “If you aim at nothing, you will hit it every single time.” – Zig Ziglar

- “You can either play now and pay later, or you can pay now and play later. The choice is yours.” – John C. Maxwell

- “The question is not, ‘Can I afford this?’ The better question is, ‘How can I afford this?'” – Robert Kiyosaki

- “Early to bed, early to rise, keeps you healthy, wealthy and wise.” – Benjamin Franklin

- “Annual income twenty pounds, annual expenditure nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pound ought and six, result misery.” – Charles Dickens

- “What good will it be for someone to gain the whole world, yet forfeit their soul?” – Matthew 16:26 (The Holy Bible – NIV)

- “Act your wage.” – Dave Ramsey

- “The principles of money are basic: Live on less than you make and save money for a rainy day.” – Anonymous

- “People buy things they cannot afford to impress people they don’t even like.” – Attributed to various people

- “Your pay raise becomes effective when you are.” – Anonymous

For more great money quotes, visit this great page.

Do YOU have any favorite money quotes? Please share them in the comments!

5 Things Money Can Not Buy

We all know that money can’t buy us everything. It can’t buy love, true happiness, or ensure a stress-free life.

Here is a list of five (frustrating, humorous, maddening) things I’ve discovered money can not purchase.

5 Things Money Can Not Buy

- A toilet that will never stop up, overflow, or leak. It will leak, hiss, or overflow at TERRIBLE times (which is pretty much any time a toilet messes up)

- Rain. I’ve lived in South Carolina for most of the past 15 years. Our local lake (reservoir) has ALWAYS been in some level of drought condition. Money couldn’t buy rain. Of course, this summer we’ve hardly had a day without rain and the reservoir is bursting at the seams.

- Children who obey perfectly. Turns out that a 3 year old will be a 3 year old whether or not you have money. Can I get an “Amen” from some parents?!?!?

- A car that won’t break down. I’ve had nice cars, and I’ve driven scary bad cars. Like 1981 Datsun B-210 bad. I’ve discovered ALL of them break down. One of my vehicles just started to have a “brake squeal.”

- Print cartridges that never run out. My print cartridge arrives at empty with impeccable timing – right when we must have it to finish the seven hour assignment from the teacher who believes a bridge built out of toothpicks somehow equals practical real world experience.

Any other frustrating, humorous, or maddening things you can think of that money can not buy? Please share!

Do I Have Enough Money To Retire?

“Do I have enough money to retire?”

This is one of the top questions I receive. It is usually asked by someone who is deciding when to retire, and they want to be financially prepared.

Let’s define retirement from the perspective of most people.

retirement date n. that moment when a person ceases to earn money and begins living on money from other sources – sources which include social security, pensions, retirement savings plans, and other investments.

Let’s back to the question – “Do I have enough money to retire?” The hidden message behind the question is, “I don’t want to run out of money and end up eating dog food to survive.”

Here’s the rough step-by-step calculation I use that can help you answer this question:

- Determine your monthly guaranteed income (social security, pensions, annuities, rental income, business income, etc.)

- Determine your monthly expenses (include savings for known upcoming non-monthly expenses like Christmas, vacation, car repairs, house repairs, annual insurance premiums, etc. Be sure to include even longer term expenses such as vehicle replacement and major appliance replacement.

- Subtract #2 from #1. This will determine your “monthly financial gap” (if one exists). If you have no gap, congratulations! You are in great financial shape. If there is a monthly financial gap, continue to step #4.

- Multiply the “monthly financial gap” by 300 – This is your “projected investments required” to provide enough income for the gap.

- Add up the total value of all of your investments – retirement savings plans, stocks, mutual funds, etc. and compare to the number calculated in step #4. If the total value of your investments meets or exceeds your “projected investments required,” you are in the financial position to retire!

Here’s an example:

Suppose Tom and Mary are preparing to retire. They are eligible for Social Security monthly payments of $2,875. They also have a small pension that will pay $300 per month. Their monthly expenses, including savings for short and long term known upcoming non-monthly expenses, are expected to be $4,500 per month. They have saved up $450,000 in their retirement savings plans – 401(k), 403(b), and Roth IRA.

Let’s use the steps to see how much they need to have saved to retire well.

- Step 1 Monthly guaranteed income is $3,175

- Step 2 Monthly expenses are $4,500

- Step 3 Monthly Financial Gap is $1,325

- Step 4 The “Monthly Financial Gap” is multiplied by 300 which provides a “Projected Investments Required” of $397,500

- Step 5 Because they have have $450,000 in their RSPs, they appear to be in great shape!

A few notes:

- This is a rough calculation. I encourage any person who is preparing to retire to meet with a retirement specialist to walk through individual needs.

- It is appropriate to understand taxes to ensure that money is utilized in the most tax-efficient manner. Using the services of a retirement specialist and CPA can help with this.

- Ensure that appropriate insurance is in place. This includes consideration of long-term care insurance and life insurance policy analysis.

- This calculation essentially assumes a 4% nest-egg growth rate that provides necessary income and preserves capital.

The Definition of Investing

I recently conducted a survey and received hundreds and hundreds of responses. One of the questions I asked was:

Which (if any) of the following financial areas do you feel CLUELESS about?

The top response was Investing.

With phrases like mutual funds, ETFs, stocks, bonds, brokers, margin accounts, rate of return, yield rate, P/E, market capitalization, and current ratio, it can literally feel as if investing is another language!

I know the feeling as I’ve been there! Because of the results of this survey, I am tasking the I Was Broke. Now I’m Not. team to aggressively address this issue. We are hard at work developing resources that are going to help take people from “clueless about investing” to “financially confident and competent investor!” You will be seeing these resources being released over the next several month, and we can’t wait to share them with you!

In the meantime, let’s start by presenting a working definition of “investing.”

Investing Using your money and possessions to create more money and possessions.

The goal for any investment is to gain more in return. There are countless ways to do this, and we are creating resources to help people maximize their investing efforts.

I look forward to sharing more in the very near future!

SERIES: Investing Fundamentals Part 4 – Unleash the Power of Compound Interest

Welcome to the latest series at JosephSangl.com – “Investing Fundamentals” Investing is consistently rated by our audience as one of the most confusing topics they face. In this series, we are going to share some foundational principles that can really help you understand investing better!

Four Unleash the power of compound interest

Compound interest is the payment of money to you from companies you have allowed to use your money.

For example let’s say we have $100 in an investment account that grew to $105 in one year. This is the equivalent of 5% interest.

Now suppose the $105 is left alone for another year and continues to grow at a rate of 5%. Will it be paid another $5 interest when the second year is up? No! It will be paid $5.25 because interest was received on $105 – not just $100. In other words, the interest money also earns interest! This is why you hear people say, “My money is working for me.”

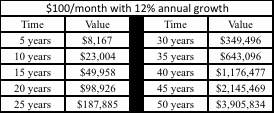

Take a look at the below example of a $100/month investment growing at an annual compounded rate of 12%.

Remember you are only investing $100 each month! Even though after 40 years you will have only invested $48,000 of your own money, your account balance will be $1,176,477! This means that $1,128,477 is the interest you have gained!

Now do you see the POWER of compound interest?

Where do you find investments that offer 12% return? I have found no investments that return 12% every single year, but I have found several mutual funds that average over 12% return over the past 50 years. Some years could lose 15% while others could gain 30%. You can see a list of my current investments HERE.

How to maximize your investment growth:

- Invest enough to receive the entire company match. By investing in an employer-sponsored retirement plan that matches some of your contributions, you could even receive a 50% or 100% return!

- Monitor your investments at least every six months. I track my investments at the end of every single month. This helps me understand how each one is performing and allows me to make necessary adjustments.

- Consider investments beyond the stock market. The stock market is just one place to invest. Consider small businesses, real estate, and intellectual property – like patents and licensing rights. Remember a higher interest rate almost always means a higher risk.

STEP TO TAKE:

- Establish a consistent investing habit. Invest every single paycheck into your retirement account for the rest of your working life. Even if you can only invest a small amount, it will add up to more than you can imagine!

RECOMMENDED RESOURCE:

- OXEN – The KEY to an Abundant Harvest In this book, Joe shares the steps you can take to maximize your money through investing!

- This book is also available via Amazon and Kindle.

NOTE: This post contributed by IWBNIN intern – Craig Fatt