Posts by Joseph Sangl

One Share of US National Debt

This is a guest post by IWBNIN team member, Mark Asbell.

It is very frustrating to see the US National Debt total consistently going up up and up with little to no plan for ever being able to fix it. When Joe updated everyone in March about the new total US National Debt, I caught myself in the middle of a very disturbing thought and emotion.

It isn’t difficult to understand that the number is going up up and up, but the number is SO LARGE I can’t even begin to really comprehend it. Throw all the analogies my way about how it would take so many hundred dollar bills that it would fill up the ocean or whatever – I still can’t really wrap my mind around $14,000,000,000,000 (trillion).

In March Joe posted how much $14 trillion translates for each of us as individuals if we all split it evenly. The number is over $46,000 per person in the US. I can understand $46,000, in fact I had heard a number like that before. When I read that my portion of the bill was only $46,000 I caught myself literally thinking “my part hasn’t gone up that much since the last time I heard that number”, and I felt as though it wasn’t so bad. That is a ridiculous thought to have, and it reminded me of a tragic flaw in the thought process I once had with my own personal finances.

For several years, my wife and I racked up a horrible amount of debt. I never dreamed we would ever get behind on bills but we did. As I think back on those times, I realize part of the problem was I would get a credit card bill, see the balance going up by large amounts and think “dang”. But then I would see the minimum payment only go up a little bitty bit and I would think, “I can handle that for now and pay it off later.” Fast forward a year or two – the same credit card balance was still going up and the minimum payment was eventually getting beyond my means. I eventually had to reach a breaking point to turn things around.

My family almost lost everything when we hit our breaking point. It doesn’t have to be that way for our personal finances OR our national finances. We should be more concerned with what the OVERALL TOTAL US Debt is and take it VERY seriously that our share is going up a little bit more every day. How long will it take for us to view that number as beyond our means? What is the breaking point going to be for our Nation?

Financial Advice to Married Persons

Financial Advice to Married Couples

o Work TOGETHER on your finances!

o Discuss all major purchases BEFORE making the purchase.

o Share ALL FINANCIAL INFORMATION with each other.

o No financial secrets.

o If you work TOGETHER, it will make you stronger.

o Avoid the trap of debt

o Some couples shell out thousands just for their marriage!

§ It is nice to have a great wedding, but to go into debt to do it?

§ Is it worth it?

o After many couples get married, they attempt to get everything that their parents have:

§ House

§ Furniture

§ Cars

§ Boat

o As a result, the first thing they have done as a couple was to strap themselves down under a weight of payments.

o Develop a plan for your future. Make your financial plan support your future plan!

o I recommend that a newlywed couple WAIT at least one year before making any large purchases (> $1000).

o SAVE money for emergencies.

o When you have no savings, every little thing that happens wrong to you (car problem, appliance problem, medical bill) becomes a financial emergency.

o Financial emergencies lead to STRESS.

o With 3 – 6 months of savings JUST SITTING THERE, these financial emergencies will not exist and therefore the stress will also not exist.

o SAVE money for the future!

Ask the following questions:

o Is the fact that you are going to retire someday unknown?

o Is the fact that your children are going to college someday unknown?

o Is the fact that your children are going to get married someday unknown?

o Is the fact that you are going to purchase a house someday unknown?

o Is the fact that you want to go on a nice vacation to Hawaii someday unknown?

o Is the fact that you want to buy a nice boat someday unknown?

o Is the fact that you want to own a nice car someday unknown?

o Is the fact that you want nice furniture someday unknown?

o NONE of these questions are unknown, yet many of us NEVER EVEN BOTHER TO PLAN FOR THEM!!!! The result of NOT PLANNING? They either go ahead with these goals and incur a TON OF DEBT OR they are unable to realize their dreams and instead live a lifetime of woulda, coulda, shoulda regret.

o Pay cash for purchases.

o Saving money takes time.

o Time allows you to truly understand if you really want that item

o It also allows you time to learn what a good deal is for that item

o Hold each other accountable.

o When one of you gets the I want this!!!-itis, the other can calm you down!

o You are stronger TOGETHER.

o Remember: ISOLATION = DESTRUCTION

o HAVE FUN WITH THIS!!!

o Managing your money can be fun. Done correctly,

o It allows you to support VERY WORTHY causes that you strongly believe in!

o It allows you to save more than you ever thought possible.

o It allows you to spend more than you ever thought possible.

o It allows you to give more than you ever thought possible.

Systematic Savings & My 529 Plan

{kind=link}

“Was it really 4 years ago that we last talked?”

“Our 20 year high school class reunion is THIS YEAR?!?!!”

Time has remained constant, but as we grow up we get so busy that it really does appear that time flies by!

It was almost 7 years ago that my daughter was born. WOW! I can not hardly believe it. In just 11 years, she will be off to college. UNBELIEVABLE!

Wait a minute … Off to college … Have I started saving for that?

The answer for us is YES!

Here is what we have done to save for her college. We started up a 529 College Savings Plan. It was VERY EASY. I went to our local bank and asked to open a 529 College Savings Plan.

Facts about the 529 College Savings Plan I am involved in:

- They required a mere $50 minimum amount to open the account.

- Additional future contributions were required to be at least $25.

- They ZAP my bank account once a month with an amount I have told them to deduct.

- The money is invested in mutual funds that I have selected.

- The money is put in AFTER-TAX, but I am able to withdraw the money (principal PLUS interest) TAX-FREE for my daughters qualified educational expenses.

- I am ONLY allowed to contribute $298,770 to this account at this time (I suspect that this will pay for college 🙂 )

- Qualified expenses included tuition, fees, books, supplies, equipment, room and board.

- If I withdraw the money for non-qualified expenses, the interest earned is subject to income taxes PLUS a 10% penalty.

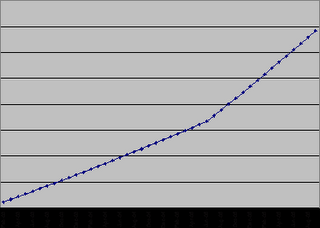

Do you know how easy it is to contribute a monthly amount to savings when you do not have to do anything? No writing checks. No on-line bill payment. Nothing. It is removed from my checking account automatically, and it is deposited into the 529 account automatically. It is then automatically used to purchase additional units of the mutual funds I have selected.

How sweet is that? Here is an example of what has happened to my 529 plan since it was started in 2003.

There is POWER in writing things down!

Have you ever told someone that you would do something, and then forgot to do it? That has happened to every one of us.

I remember going to visit a customer that had experienced a quality issue with one of our products. I had a belief that we had not been notified in a timely manner about the quality issue. I was WRONG. This customer pulled out a book and rattled off at least 10 times that he had contacted our team about this exact issue! He had NAMES. He had DATES. He had TIMES. He had the Greenwich Mean Time in which he had contacted them. He had EXACTLY what he had relayed to each individual. There is POWER in writing things down!

By the time he had gotten to relaying to me the fourth call he had made, I really was not interested in hearing any more! I just wanted OUT OF THERE. Why? Because I did not have it written down. My team had not written it down. As a result, we had seriously inconvenienced a customer, and we had look foolish doing it. There is POWER in writing things down!

With this blog, I embarked on a journey to write about personal finances. I wanted to help others improve their own personal financial situation. The end result? I am personally learning more about finances. Why? Because I am writing it down!!! There is POWER in writing things down!

God had approximately 40 authors WRITE THINGS DOWN. Why? Because there is POWER in writing things down!

Write things down! Use the POWER!

Moving Costs – If you ever move …

Moving costs money.

Surprised?

Here are some questions (answers below):

- How much does it cost to rent a one-way 26′ box truck for 5 days and unlimited miles?

- How much does it cost for boxes?

- How much does it cost for the fuel to get from point A to point B?

- How much does it cost to rent a car tow dolly?

- Have you thought about furniture pads?

- How much does it cost to get your old house ready to move out of?

- How much does it cost to get your new house ready to move in to?

- If you are selling your home, how much does it cost?

- One-way rentals are FAR more expensive than returning the rental to the spot you picked up the truck. General costs for a one-way rental is between $1,300 and $2,500.

- Boxes. Wow. Moving boxes that you purchase run anywhere from $150 – $500.

- Fuel? Depends on the average gas prices. 26′ box trucks get HORRIBLE gas mileage – between 4 and 7 mpg. If you get a diesel, you can expect to get between 8 and 12 mpg.

- A car tow dolly will run you around $200

- Furniture pads are very cheap. Around $10/dozen. Get at least two dozen more than you think you will need.

- Depends greatly on the condition of the home. If you’ve maintained things well, it could be $500 or less. If you haven’t maintained things well, it could be a LOT more.

- Depends greatly on the condition of the home. If you negotiate effectively, you can have the house handed over in great condition.

- If you use a realtor, selling fees on a home generally run between 4% and 7%. If you sell your home yourself, you can do it for somewhere around $1,500.