Budgeting

Known, Upcoming Non-Monthly Expenses Calculator

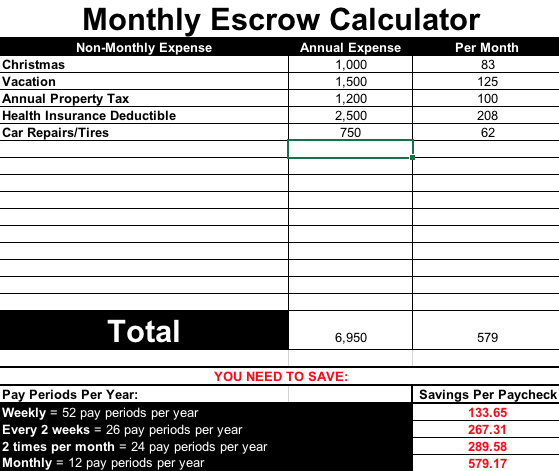

Have you ever prepared a budget and faithfully followed it only to have it crushed in the middle of the month because of an expense you forgot about? Does Christmas seem to creep up on you every year? Have you had to suddenly replace the tires on your car? Chances are, you answered yes to at least one of these questions.

These budget busters are called “Known, Upcoming Non-Monthly Expenses.” The reason these expenses get forgotten is because they are non-monthly so they tend to be pushed to the back of the mind until the bill suddenly comes in the mail. But when they do finally appear, they can create a financial emergency causing you to either break your budget or go into debt.

Think about what non-monthly expenses you know will come up throughout the year. Here are a couple of common expenses that people have:

- Car tires need to be replaced

- Heating & Air goes out

- Christmas

- Vacation

- Life insurance premium

- Property taxes

- Health Insurance deductible

Once you have these expenses listed out, you can plan to save monthly for them in your regular budget. Check out our Known, Upcoming Non-Monthly Expenses Calculator to do this with ease. Below is an example of the calculator in action:

By knowing what these expenses are and saving for them monthly, you’ll no longer have to “come up” with the money when the bill arrives. You will simply be able to pay the bill in cash. A cool feature of this tool is that not only does it calculate what you would need to save per month, but it also calculates the amount based on different pay frequencies. If you get paid twice per month, you would need to save $289.58 out of each paycheck. For a bi-weekly frequency, you would save $267.31. Regardless of how often you get paid, you can save accordingly and have the money available when you need it.

Tips for using the tool:

- Be sure to recalculate your monthly savings number at least once per year.

- Don’t forget more long-term expenses such as college, weddings, vehicle replacement, and major home renovations.

- Make your savings for these expenses AUTOMATIC by establishing an auto-draft.

========================================================================

Want more tips like this one? Subscribe to the Monday Money Tip Podcast HERE.

How To Have A Debt Free Christmas

What if I told you that you don’t have to go into debt Christmas shopping this year? That you can buy your gifts IN CASH and can avoid those dreaded credit card bills in January? Can you guess how you accomplish this? That’s right, a budget.

Christmas is a known, upcoming, non-monthly expense. That means that we know that Christmas comes on the same day every, single year and we should plan for it accordingly! In the Sangl household, we do this by saving a little bit for Christmas each month.

First, we decide how much we want to spend on Christmas altogether. Then, we create a list of every person or organization that we’re planning on buying a gift for and decide how much we plan to spend on each person. All that’s left to do is make that budget equal EXACTLY ZERO. Once you have your plan put together, you can do your Christmas shopping guilt-free!

You can download a copy of one of our FREE BUDGET TOOLS HERE.

========================================================================

For more tips on how to have a debt-free Christmas, check out our full episode of the Monday Money Tip Podcast HERE.

For more information on how to create a Christmas Mini-Budget, check out this related blog post.

All About the Budget Challenge!

There was a time in my life that I was completely clueless about money. My life was a financial mess. I had massive amounts of credit card debt, huge student loan balances and to top it off, I decided that I needed to purchase a brand new car and home. I was on a downward spiral, and I needed to make some drastic changes, and fast.

Then, Jenn and I decided to prepare (and follow!) a budget. It sounds so incredibly simple but it changed our financial future. One hundred eighty-two months ago, my family prepared our first ever budget and have followed one every month since.

I know that many people have felt the same way that I initially did about my finances. I know because I asked. Here is what people told us about budgeting:

- 37.5% said their budgets do not work because they do not know how to budget effectively.

- 27.5% of people said budgeting was “too frustrating and emotional” so they just gave up.

- 25.8% felt like they did not make enough money so there was no point in creating a budget.

- 27.5% said there “just was not enough time in the day” so they gave up.

- 18.3% of people said they could not budget because their spouse would not participate.

Can you identify with any of this? If so, I’m excited to tell you that I have a solution! I know that many of you need help with budgeting so I have taken some time and created the I Was Broke. Now I’m Not. Budget Challenge. This 40-day challenge will equip you with everything you need to finally master your money.

Challenge Info:

- When does the challenge begin? It will kick off with a LIVE two-hour, online equipping event on Tuesday, August 21st.

- How does it work? You will receive special teaching EVERY DAY of the challenge! The first 10 days will focus on preparing your actual monthly budget for September. The final 30 days will help you succeed with your budget throughout the month.

- Can I get real help from the IWBNIN team? Absolutely! There will be a live call once per week on Thursday at 8PM EST where your questions will be answered by Joe or a member of the IWBNIN team.

- Do I have to show up to the live events or will they be available on-demand? We understand that you have a busy life! To help accommodate you, we will record all live events and make them available to all 40-Day Budget Challenge Participants!

If you have had enough and you are ready to take control of your money, reduce financial stress, and start making progress toward your plans, hopes and dreams, join me on the 40-Day Challenge. Do not miss this opportunity! REGISTER HERE!

Money Lies – I Can’t Budget

There are tons of excuses for why you should not budget. It is hard, it can be time consuming, and you might not feel like you make enough to budget. I get it. But if you have been believing any of these excuses and use it as a reason why you cannot budget, you are believing a lie! I am not going to lie to you, budgeting can be challenging. If it were easy, people would not feel so intimidated by it.

Ultimately, budgeting or not budgeting is a choice. There is not a situation that prevents you from completing a budget. You either choose that you are going to win with your money or you choose to let your money run you. I know which option I am choosing. A budget allowed me to do so much more than I ever thought possible in terms of my finances. A budget set me free.

- A budget allows me to know where every single dollar is going BEFORE I am ever paid.

- A budget provides me choices – because I plan it before I receive it.

- A budget allows my bride and I to have constructive conversations every single month about our plans, hopes and dreams.

- A budget allowed me to pay off all of my non-house debt in just 14 months.

- A budget allowed me to pay off my house in 10 years and 1 month.

- A budget allowed me to send my daughter off to college without incurring any student loans, fulfilling a dream of mine.

You can come up with as many reasons as you would like to not budget. But, there are so many more reasons that you need one! It will set you free and allow you to do more than you ever thought possible, just as it did for me.

Try some of these practical ways to make a budget work well for you:

- Use a budget tool – Budget tools will do the math for you. This keeps you focused on the financial decisions at hand instead of facing a terrible math quiz. You can try our FREE BUDGET TOOLS HERE and they will do all the work for you!

- Build an emergency fund equal to a full month of EXPENSES – Notice I said expenses, not a full month of your income. Once you have saved enough for an entire month of expenses, you can ignore multiple paychecks and use the Monthly Budgeting Tool instead. And, you will rid yourself of a level of stress that you may not have even known you had!

- Be realistic – If you are just beginning to prepare a monthly budget, it is important to be realistic about your expenses. Do not tell yourself that you will spend $3.45 on groceries in the next month. That is not possible and you will fail if you structure your budget this way. If you have a household of kids that are involved in 62 after-school activities, do not put $0 in your dining out budget. Go through your debit/credit card history and see what your spending habits are. Once you have determined what your history is, you can trim to what is reasonable.

Remember, no matter how daunting of a task you think budgeting is, it is going to beat not budgeting 10 out of 10 times. Do it. You need it.

==============================================================================

Want more tips like this one? Subscribe to the Monday Money Tip Podcast HERE.

Are you struggling with your budget? Are you ready to take control and finally start winning with your money? If so, join our first ever I Was Broke. Now I’m Not. 40 Day Budget Challenge. During this challenge we will help you create a budget and give helpful and practical tips every single day to make sure that you follow through until the end of the month. Our launch date is Tuesday, August 21st and you can REGISTER HERE. Don’t miss out!

Mini Budget Tool – Plan your back to school spending!

Can you believe it is already August?!! Summer has flown by and school is right around the corner. With classes starting up, inevitably you will be getting a list of required school supplies that your child will need for the first day of school. You planned for that in your budget, right?

You should have set aside some money for school supplies and new clothes but the Mini-Budget Tool can help you take that planning one step further, especially if you have multiple kids!

You can use the tool to show different scenarios for spending different amounts on various items. Get your list(s) together and make a plan for your back-to-school shopping. This way, you are way less likely to overspend and blow your August budget.

Remember, when your INCOME – OUTGO = EXACTLY ZERO, the cell will turn green, indicating that you have “spent” every dollar on paper first. You will notice after you download the tool, there are three different options for your budget. This gives you the option to spend your money multiple ways and see which allocation of money makes the most sense for you.

Try out the mini-budget tool today and plan your back to school shopping today!

EXTRA TIP: Make sure you check to see if your state participates in Tax Free Weekend and plan your school shopping then! This can be really helpful in saving some money, especially if you are looking to buy big ticket items such as a new laptop!

========================================================================

Want more tips like this one? Subscribe to the Monday Money Tip Podcast HERE.