Finance

SERIES: Sell Car With Negative Equity – Part 1

Welcome to the latest series – "Sell Car With Negative Equity"

The fact that most cars drop in value by sixty percent in the first four years causes an enormous part of the American population to struggle with huge car payments and an inability to rid themselves of the car without acquiring yet another new car and rolling in the negative equity to the new loan.

It is my hope through this series, that you will be equipped to sell a car that has negative equity.

Part 1 – Recognize How Much A Car Really Costs

Some of the actions in this series might be difficult to execute, but when one recognizes how much a car really costs it can really help solidify sound financial decisions.

I believe that having a car payment is a HUGE financial mistake. Here is why.

First, cars drop in value. New cars drop in value FAST. Most new cars drop in value by around sixty percent in the first four years. This is called depreciation, and it causes one's net worth to drop.

Second, car payments reduce one's ability to gain financial freedom. Loan interest can range from 0% to 20% or higher depending upon one's credit. Even 0% loans are negative financial events because the money is going toward a car that is dropping in value. What else could one do with a monthly car payment? Give more? Invest more? Spend more?

When I recognized how much my debt was costing me, it solidified my commitment to achieving financial freedom. I was so dad-blamed sick of debt and what it was doing to my family.

Read the entire "Sell Car With Negative Equity" series HERE.

Receive each post automatically in your E-MAIL by clicking HERE.

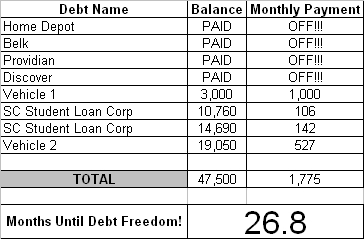

Marching To Debt Freedom – Couple #3 – Month 09

Introduction

This couple has been married for many years and have one child. They have HAD IT with their debt and have been marching toward debt freedom since November 2007. They are THROUGH with credit cards.

Good things this month

We transferred JC Penney balance which was 21.99% to a 2.9% on Discover AND we transferred Chase that was 26% to a Juniper Mastercard at 7.9%. We were VERY excited about those transfers.

It is also very encouraging to see the balance on the National City card come down!! It won't be long until that one is GONE!

Challenges this month

Challenges this month have been the rising cost of gas and food, but we have just budgeted a little differently in some areas and made it work out fine! Again, this month I have to say THANK GOODNESS for the budget form!!! We were able to pay cash for all back to school items this year and MAN! Does that ever feel good!!!

Updated Debt Freedom Date …

Month By Month Progress …

![]()

Sangl Says …

It is so nice to see Couple #3 reap the rewards of the hard work they put forth to restructure their debt. Look at the tremendous progress they are making. Instead of twenty percent of their payments going toward principal and eighty percent to banks, they have switched it around. Now, over 80% of all of their payments are going toward principal reduction! AWESOME!

Readers …

If you have debt, have you considered restructuring it? This can really help your debt freedom march gain a ton of traction and speed up your journey to ZERO DEBT! I encourage you to read the series of posts I wrote called Restructuring Debt.

My book, I Was Broke. Now I'm Not, is available via AMAZON.COM, BORDERS.COM, and PAYPAL. You can read the Introduction HERE. In this book, you will learn exactly how Jenn and I became debt-free in just fourteen months.

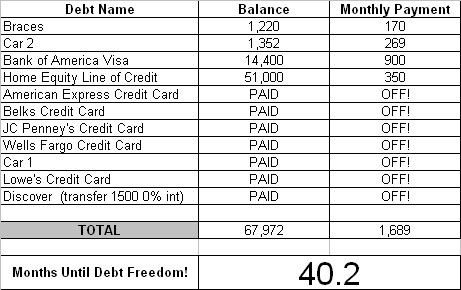

Debt Freedom March – Couple #2 – Month 12

Introduction

This couple is THROUGH with debt! They announced that they were breaking up with debt in October 2007. They have agreed to share their Debt Freedom March with everyone in the hopes of inspiring others to do the same!

Here is this month's update.

Here is their updated Debt Freedom Date calculation …

Month By Month Progress …

![]()

Sangl Says

This is the one year anniversary of Couple #2's Debt Freedom March and look at how much debt they have paid off! They started out in the $70,000 range and are now in the $40,000 range. They have paid off $24,410 in ONE YEAR!

I am so excited for Couple #2. They are being blessed financially and instead of running out and blowing all of it, they are using it as an opportunity to completely change their entire financial future!

Marching To Debt Freedom – Couple #1 – Month 12

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now ELEVEN months into their Debt Freedom March.

Good/Bad This Month

This month went to plan. It is great to see these balances going down. On the other hand, it is difficult for expenses to go up so much. It seems as though all of our extra spending money is going in the tank and into the grocery cart, but I can't complain. I feel very lucky. We have a house that is not in foreclosure, and we have two great jobs with benefits and insurance. We are so blessed.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Couple #1 is now twelve months into their debt freedom march. What a fantastic year it has been! They have paid off $21,801. This is what can happen when one is intensely focused on debt freedom and recognizes what life will be like when there is ZERO DEBT.

When Couple #1 started out, they had $35,695 in non-house debt. They now have only $16,000 of non-house debt remaining. Outstanding!

Couple #1 is doing a great job of sticking to their debt freedom march. There are times that it seems almost unattainable, but it IS attainable and it IS so worth it!

Readers …

How is your own Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction HERE.

Receive each post automatically in your E-MAIL by clicking HERE.

SERIES: Restructuring Debt – Part Six

Welcome to the latest series at JosephSangl.com – Restructuring Debt

Welcome to the latest series at JosephSangl.com – Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Part One – Know What You Are Paying

Part Two – Lower The Interest Rates!

Part Three – Lower The Interest Rates! – Continued

Part Four – Lower The Interest Rates! – Continued

Part Five – Lower The Interest Rates! – Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, it was the debt consolidation option. In Part Five, it was the credit score option. In Part Six, I will be sharing my most favorite way to restructure debt.

Part Six – CRUSH IT, SMASH IT, HAMMER IT, DESTROY IT

I used to be broke. I used to have $4.13 in my bank account after paying all of my bills, and I was pumped because it was a positive balance. Yet, I was sending hundreds of dollars every single month to banks for debt. I finally experienced my I Have Had Enough Moment (IHHE Moment) and attacked my debt.

I know that the interest is annoying. I know that trying to get the lenders to lower their interest rates is frustrating and humiliating. Besides that – much of that is out of our control. But controlling how we spend our money from now on IS in our control. Not signing up for more debt IS in our control. Going to work for sixteen hours a day to eliminate our debt superfast IS in our control. Selling our car, boat, truck, collectibles, and other niceties IS in our control. No, it might not be fun, but paying hundreds and thousands of dollars a year in interest is MISERABLE and robs us of the ability to go do EXACTLY what we have been put on this earth to do!

So I end this series with two questions and their answers.

Q: How much interest do you have to pay when you have zero debt?

A: ZERO

Q: How much interest is paid to you when you have money in the bank or invested?

A: Anywhere from 3% to 12% or more! Paid TO you! I decided long ago to choose to have interest paid to me instead of paying it to someone else.

I trust that this series has helped you. I love hearing the stories. If you would be willing to share your story or would like to sign up for a free financial counseling session with one of our fifteen trained volunteer counselors, fill out the contact form HERE.