Posts by jsangl

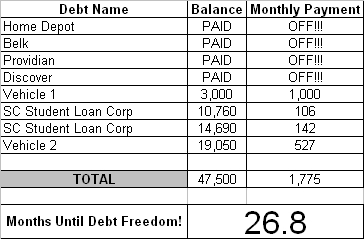

Debt Freedom March – Couple #2 – Month 12

Introduction

This couple is THROUGH with debt! They announced that they were breaking up with debt in October 2007. They have agreed to share their Debt Freedom March with everyone in the hopes of inspiring others to do the same!

Here is this month's update.

Here is their updated Debt Freedom Date calculation …

Month By Month Progress …

![]()

Sangl Says

This is the one year anniversary of Couple #2's Debt Freedom March and look at how much debt they have paid off! They started out in the $70,000 range and are now in the $40,000 range. They have paid off $24,410 in ONE YEAR!

I am so excited for Couple #2. They are being blessed financially and instead of running out and blowing all of it, they are using it as an opportunity to completely change their entire financial future!

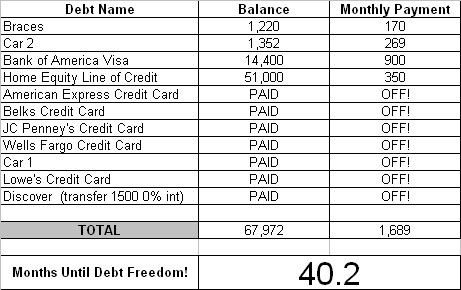

Marching To Debt Freedom – Couple #1 – Month 12

Introduction

Couple #1 is THROUGH with debt! They have been married for many years and have two children. They are now ELEVEN months into their Debt Freedom March.

Good/Bad This Month

This month went to plan. It is great to see these balances going down. On the other hand, it is difficult for expenses to go up so much. It seems as though all of our extra spending money is going in the tank and into the grocery cart, but I can't complain. I feel very lucky. We have a house that is not in foreclosure, and we have two great jobs with benefits and insurance. We are so blessed.

Updated Debt Freedom Date

Month By Month Progress

Sangl Says

Couple #1 is now twelve months into their debt freedom march. What a fantastic year it has been! They have paid off $21,801. This is what can happen when one is intensely focused on debt freedom and recognizes what life will be like when there is ZERO DEBT.

When Couple #1 started out, they had $35,695 in non-house debt. They now have only $16,000 of non-house debt remaining. Outstanding!

Couple #1 is doing a great job of sticking to their debt freedom march. There are times that it seems almost unattainable, but it IS attainable and it IS so worth it!

Readers …

How is your own Debt Freedom March progressing?

In my book, I Was Broke. Now I'm Not., I share the story of my Debt Freedom March and teach the exact tools that Jenn and I used to become debt-free. You can do it too! You can read the book's introduction HERE.

Receive each post automatically in your E-MAIL by clicking HERE.

SERIES: Restructuring Debt – Part Six

Welcome to the latest series at JosephSangl.com – Restructuring Debt

Welcome to the latest series at JosephSangl.com – Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Part One – Know What You Are Paying

Part Two – Lower The Interest Rates!

Part Three – Lower The Interest Rates! – Continued

Part Four – Lower The Interest Rates! – Continued

Part Five – Lower The Interest Rates! – Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, it was the debt consolidation option. In Part Five, it was the credit score option. In Part Six, I will be sharing my most favorite way to restructure debt.

Part Six – CRUSH IT, SMASH IT, HAMMER IT, DESTROY IT

I used to be broke. I used to have $4.13 in my bank account after paying all of my bills, and I was pumped because it was a positive balance. Yet, I was sending hundreds of dollars every single month to banks for debt. I finally experienced my I Have Had Enough Moment (IHHE Moment) and attacked my debt.

I know that the interest is annoying. I know that trying to get the lenders to lower their interest rates is frustrating and humiliating. Besides that – much of that is out of our control. But controlling how we spend our money from now on IS in our control. Not signing up for more debt IS in our control. Going to work for sixteen hours a day to eliminate our debt superfast IS in our control. Selling our car, boat, truck, collectibles, and other niceties IS in our control. No, it might not be fun, but paying hundreds and thousands of dollars a year in interest is MISERABLE and robs us of the ability to go do EXACTLY what we have been put on this earth to do!

So I end this series with two questions and their answers.

Q: How much interest do you have to pay when you have zero debt?

A: ZERO

Q: How much interest is paid to you when you have money in the bank or invested?

A: Anywhere from 3% to 12% or more! Paid TO you! I decided long ago to choose to have interest paid to me instead of paying it to someone else.

I trust that this series has helped you. I love hearing the stories. If you would be willing to share your story or would like to sign up for a free financial counseling session with one of our fifteen trained volunteer counselors, fill out the contact form HERE.

SERIES: Restructuring Debt – Part Five

Welcome to the latest series at JosephSangl.com – Restructuring Debt

I am excited to embark on this series of posts because interest paid toward debt is one of the largest obstacles to gaining traction for one's own Debt Freedom March.

Of course, one way to eliminate the interest is to sell some stuff and become debt-free. But I recognize that for some people, they have debt that they are going to have to focus on and just pay it off. If this describes you, then I trust that this series helps you gain speed in your Debt Freedom March!

Part One – Know What You Are Paying

Part Two – Lower The Interest Rates!

Part Three – Lower The Interest Rates! – Continued

Part Four – Lower The Interest Rates! – Continued

There are many approaches one can take to lower their interest rates. In Part Two, I covered the "negotiation" avenue. In Part Three, we covered surfing the balances to zero-percent credit cards. In Part Four, it was the debt consolidation option. In Part Five, I will be covering the credit score option.

Credit Scores Matter!

I know. I am brilliant. But it matters so much when it comes to reducing the interest that lenders will charge on your existing debt (this is a no-new-debt zone!). As your credit score improves, your credit card surfing and bill consolidation loan options will improve.

There is a company that actually specializes in consolidating loans for people with excellent credit. I was told about this company by a banker friend who has been extremely impressed with the way this company is doing business. It is called FirstAgain.com. It is actually stated on their web site that "Excellent and Substantial Credit Required". No need to apply if you have trashed credit, but it looks like a good option for those who are looking restructure their debt and gain traction with their Debt Freedom March.

Of course, there are also companies that specialize in loans for people with horrible credit. Payday loan joints, title loan sharks, pawn shops, and various other organizations provide loans that have HORRIFIC interest and should never be considered a viable option for someone who expects to gain traction on their Debt Freedom March. I have yet to meet the first person who became debt free because of their rip-off payday loan. I have met hundreds who have became completely hopeless because of their rip-off payday loan.

In the sixth and final installment of the Restructuring Debt series, I will be sharing my favorite way to restructure debt.

Receive posts automatically in your E-MAIL by clicking HERE.

Winner of “Wild Goose Chase”

Wow. All I can say is, "Wow." After reading all of the terrific comments, there was absolutely no way I could choose any single one of them. So I ended up resorting to the old-fashioned "names in a hat" technique to choose the winner of Wild Goose Chase by Mark Batterson.

Wow. All I can say is, "Wow." After reading all of the terrific comments, there was absolutely no way I could choose any single one of them. So I ended up resorting to the old-fashioned "names in a hat" technique to choose the winner of Wild Goose Chase by Mark Batterson.

The winner is Casey Morgan who submitted the second comment on the review I wrote up about the book.

Congratulations to Casey, and for those who did not win the free copy, I highly recommend that you hop on over to Amazon.com and pick up a copy. You could even bundle it with a copy of I Was Broke. Now I'm Not. and qualify for free shipping!

Congratulations again to Casey Morgan for winning the free book!

Receive posts automatically in your E-MAIL by clicking HERE.