Resources

Working Together To Win With Money

When my wife, Jenn, and I began our budgeting journey, we discovered a magical ingredient for achieving financial success: working together. I want to share the benefits we’ve enjoyed since we started “working together to win with money.”

Benefit #1 – We BOTH know our financial situation.

Before Jenn and I started working together on our finances, there were a lot of episodes of unplanned spending. As a result, we would run short of cash at the end of the month and cover those shortages with credit cards. Because neither or us truly understood where all of our money was going, it led to additional financial mistakes. These would lead to unnecessary stress and frustration.

It also resulted in an average bank account balance of $4.13. Since I am an eternal optimist, I would say, “Hey! At least the balance is positive and not negative!”

We later realized our financial behavior was robbing us of our future hopes, plans, and dreams. In December 2002, we had our IHHE Moment (I Have Had Enough Moment) and said, “ENOUGH,” and stopped spending money in a wild manner. By July 2003, we had formalized our spending into a monthly spending plan (A.K.A. a budget). Ever since then, we have planned each month’s spending.

The result? We have been debt-free (except the house) since February 2004. We have achieved many of our life dreams, and we both know our financial situation.

Keys To Obtaining Benefit #1

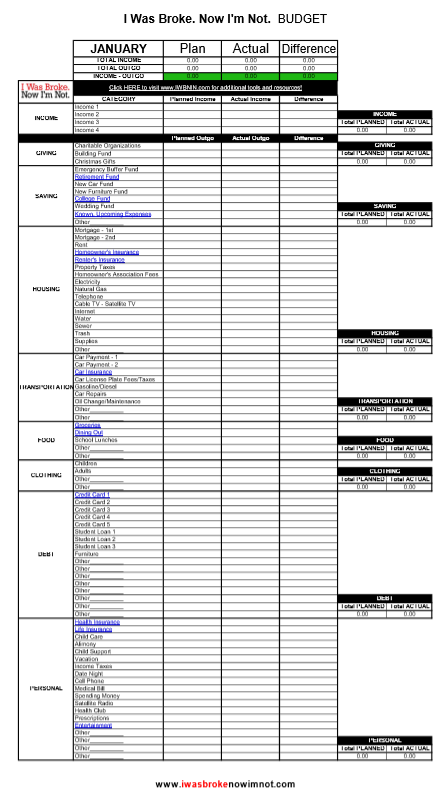

- Prepare a written spending plan every single month – visit HERE for a free budget template and check out this post “How Do I Budget?”

- This monthly rhythm will create a natural space for you to have conversation about your finances. Since nearly everything in life costs money, it will allow you to have a conversation about the more important things of life too. This is perhaps the most powerful result of preparing and following a monthly budget.

- If you have a financial mess, it is time to have an IHHE Moment

- This is the moment where you say, “Enough is enough.” It is a definitive moment where the pain of keeping things the same exceeds the pain of changing. This is a vital component of every financial turnaround as it provides energy and passion to help you power through the challenges of changing old financial habits and behavior.

- Take the time to talk with your spouse about your hopes, plans, and dreams – and write them down!

- At least once a year, you should have a focused conversation on your plans hopes and dreams. The dreams you share as well as your individual ones. This can be a wonderful time of hope and challenge that helps you remain committed to positive financial decisions.

Benefit #2 – Improved communication.

When Jenn and I were B-R-O-K-E and constantly spending money we did not have, we really had no idea where our money was going. All we knew was this: it was leaving at a very rapid pace!

By working together to win with money, our communication changed dramatically. I now know when each of my nephews and nieces have a birthday because we send them money. We can’t just magically produce the money we send them every birthday. It must be planned. Through this rhythm of monthly meetings, these gifts are carefully included into our monthly spending plan while also having a wonderful conversation about each beloved family member who is turning another year older.

We also discuss our future plans, hopes, and dreams. We talk about which dreams will be funded now and which ones will need to be funded later. Together we made a decision to fund college education for our three children. We fund that education every single month. In January 2003, we agreed together that this goal was extremely important to us, and we made it a priority.

We both have a desire to travel around the world. As such, we made a decision that most of these travels will be funded in the future, not now. However, we have focused on funding a few trips right away. We typically take a family vacation each summer where we tour several states and visit family. Living in South Carolina, we also love visiting the beach. Because of this, we have made beach trips a priority. These trips are funded monthly because they are included as an expense in our monthly budget. This allows us to pay cash for each trip without any debt following us home. This all happens because of one key reason: we have agreed together to sacrifice other items in order to fund each of these higher priority goals.

Because of our improved communication, we have been able to give more money to causes and people we believe in.

To put it very plainly: there is no possible way we are ever going back to our old way of money (mis)management. Our marriage has been vastly improved by the fact that we are working together to win with our money.

Keys to Obtaining Benefit #2

- Understand each other’s plans, hopes, and dreams.

- Few things are as satisfying as setting a goal and achieving it with the one you love. Have you written down your plans, hopes, and dreams? What about your spouse? How long has it been since you allowed yourself to dream?

- Take time to develop a written spending plan TOGETHER – free budget tools are located HERE

- Let’s face it. Budgeting is not the most exciting task you will undertake on any given day. However, when you realize that your budget, and the process of preparing it together with your spouse, is the critical and vital tool that will maximize every dollar and enable you to achieve the huge plans, hopes, and dreams of your life, you might discover that you suddenly enjoy this process in a way you did not think was possible. You will be spending your time working together to win with money

- Plan your spending EVERY SINGLE MONTH – ensure that you are funding at least one of your dreams at all times

- Have you noticed how fast time goes by? My firstborn was just entering kindergarten and now high school is already in her rear-view mirror! If you do not commit to preparing and following a budget each month, you will seemingly blink and a year (or more) will pass. Mark my words, any month you allow to pass without preparing a plan is a month you did not maximize the impact of your money.

- Become debt free – calculate your Debt Freedom Date HERE and check out this post to learn more about how “You Can Be Debt-Free”

- Have you ever known anyone who said their credit card debt was the reason for their financial success? Probably not. The same can be surely be said for furniture debt, student loan debt, and owing a friend or family member. We all understand that debt is not all created equal. Credit card debt is wildly different from a home mortgage. But consider this thought: What would your life look like if you owed zero debt except your home? What if you were completely debt-free – including your home?

Benefit #3 – Dreams Get Funded!

By working together to win with money, many of our dreams have been funded.

We have had tons of dreams … A new kitchen with granite counter tops, a new master bathroom, paying for our kids’ college education, paying cash for our kids’ first house, giving away $1,000,000, starting a university, living for a year in downtown Chicago, traveling to Australia, Europe, and Asia, owning a 100 acre farm …

Quite frankly, the list of dreams goes on and on. However, because we have talked about them and prioritized them, many of them have been fully funded. In fact, it is my belief that one hundred percent of the above goals will be funded during our lifetime. Why do I believe that? Because we have funded so many of our dreams already! Many of them were dreams we did not think were really possible when we first discussed them. It is amazing what happens when you have a financial plan and work together to win with money.

If we fail to achieve all of our dreams, so be it. It will be a blast knowing we gave our best effort together!

Keys to Obtaining Benefit #3

- Remove all distractions and take the time to have a great conversation about your plans, hopes, and dreams.

- Children are wonderful and beautiful, but there are some conversations that are better without their constant input (or interruption). One of these includes the conversation about your plans, hopes, and dreams. Schedule your conversation so you can ensure a distraction-free environment for this most important of discussions. For example, Jenn and I scheduled a three-day getaway to Charleston, SC to update our plans, hopes, and dreams. It was a wonderful time and we came back with a new perspective and dreams.

- Ask these questions of each other:

- Will these dreams cost money? How much?

- If we continue to manage money the way we are right now, will we be able to achieve these dreams?

- What is your most important dream? How can we start funding it right now?

How Working Together Has Helped Us

Ever since our IHHE Moment back in December 2002, Jenn and I have taken our financial decisions much more seriously. The addition of a budget greatly accelerated our financial success. By February 2004 (just 14 months later), we were debt-free except for our home. We have been able to launch and purchase eight companies, acquire the farm, and invest in rental real estate. At this moment, our oldest daughter is nearing completion of her college journey – with zero debt. We are so grateful for the journey and the blessings we have experienced. It is our mission and goal for you to enjoy the same success. We truly believe it is possible for you to live your own Fully Funded Life! You can do this! We believe in you.

=====================================

After more than 25 years of managing money, I finally took time to write about the profound impact that one’s plans, hopes, and dreams can have on your financial behavior. I have entitled the book, 20/20 Money: Gaining Clarity for Your Financial Future. Included within this book are 22 Vital Questions you should ask to help discern and fully understand your own plans, hopes, and dreams and just exactly a Fully Funded Life looks like for you. You can learn more and pick up your copy HERE.

Are You Stuck Financially?

Have you ever been stuck financially? I mean STUCK. Do you feel so stuck that you can’t even gain any traction to get control of your finances?

Perhaps you have no income because you have lost your job. Maybe you are in college and accumulating debt to pay for it. Perhaps your spouse spends money faster than you make it. Or maybe you are just lost when it comes to managing money. It might even be the fact that you have so much unsecured debt that you feel that the creditors should just change the amount owed to a cool $1,000,000 because it might as well be that much! Maybe you are disabled, and can’t figure out what to do to earn more money.

If this is you, this post is for you! In this post, I will be sharing steps you can take to become “unSTUCK”.

I am FIRED UP!

Step One: Why are you stuck financially?

It is important to understand why you are stuck financially. There are some situations that have definite ends to them (college) and other situations that have indefinite ends to them (job loss, disability, and overwhelming debt).

Why are you stuck?

Write it down on paper. Right now. Write “I am stuck financially because … “.

When I encounter situations where I don’t know what to do, I start writing. Writing enables me to put all of my thoughts on paper.

After writing all of my jumbled thoughts down, I set it aside for awhile. After a day or two, I revisit what I have written and identify the repetitive thoughts. This helps me identify the core issue.

Why are you stuck or what caused you to be stuck in the past?

Step Two: Plan what you have!

Now that you have written down the reasons that you are stuck, it is time to prepare a written spending plan.

Yes, a budget. Here is something I have learned – managed money goes farther than money that isn’t managed.

I know that what you have is limited. In some cases, VERY limited. BUT, it is imperative that you plan what you do have.

We offer free budget tools on the I Was Broke. Now I’m Not. website to help you start budgeting.

If you are paid once per month, this is the budget tool for you.

If you are paid multiple times per month (twice/month, bi-weekly, bi-monthly, weekly, etc.), this is the budget tool for you.

If you want to learn how to put together a great budget, you might want to read the “How Do I Budget?” post.

Step Three: Remember the priorities!

When you have an extremely limited amount of funds, it is important to remember the priorities. I have met a lot of people who have been tricked and shamed by credit card companies into paying the credit card bill instead of the house payment.

You have completed step two and planned what you do have, so now the next step is figuring out who gets paid and who does not.

My priorities are:

-

Essentials:

House payment (or rent), basic utilities, car payment, gasoline, and food. This does NOT include cable, internet, phone, restaurants, fashion clothes, etc.

-

Secured Debt:

If money remains after covering the essentials, then it is time to pay for the secured debts. If secured debts are not paid, the creditor has the right to come take the item. They will usually sell it at wholesale and come after the rest from guess who? So I would pay the secured debt next.

-

Unsecured Debt:

Creditors cannot immediately come take something from you so they can be paid later if the money runs out.

-

Fun:

This is last on the list. Besides I can have fun for free. Pickup basketball games, watching old movies, etc.

Who is the manager of YOUR money? It should be YOU! Not your creditors! YOU choose where it goes.

Even if you don’t have enough money to pay all of the bills, go ahead and put all of the bills into your spending plan. This is a KEY step! You need to clearly understand how large the gap is between your INCOME and your OUTGO.

I call this gap the “GO GET THIS” gap. That is the next step!

Step Four: Fill the “Go Get This” Gap!

I am sure that some read this as “Go work like crazy and earn more money”. I would certainly not disagree with working more and earning more! It is a GREAT way to fill in the “Go Get This” Gap.

But there are many more ways to fill in the gap! Here are quite a few.

-

Pray.

I am a Christ-follower, and I have seen the power of prayer.

-

If married, ensure that your spouse is on board.

There is POWER when you work TOGETHER on your finances! How do you get a spouse on board could be a year-long series, but it is so necessary. Jenn and I work together because we wrote down all of our earning and spending. When we saw that our OUTGO exceeded our INCOME, we knew that it was a serious issue! One strategy to try is to mail the kids off to Grandma & Grandpa’s (eliminate distractions) and tell your spouse that you want to talk to them about something that you really need them to hear. Something that is really important to you. Very important to you. And then show them your family’s finances planned out on paper. When you write out where you are stuck financially it tends to reduce the emotion towards each other. You have the opportunity to become a unified in your effort!

-

Govern your business.

If your business is struggling, it might be worth putting some “mileposts” in place. Mileposts are points one month, three months, six months, and twelve months away. An example of a milepost is “If we are at $5,000 sales in three months, we will keep the business. If it is at $3,000, we will keep it open for three more months. If it is less than $3,000, we are going to have to shut down the business.” The hardest thing in the world for an entrepreneur is to close their business. Tough, but necessary sometimes.

-

Sell something.

Maybe your house payment is eating you alive. Sell the house. It could be time to sell the motorcycle, the boat, the truck, the swing set, the four-wheeler, or the 50″ TV. Whatever you have of value that isn’t a “need” – it may be time to part with to help.

If you’re looking to sell something online check out Episode #106 of the Monday Money Tip Podcast for tips.

-

Reduce OUTGO.

Many times you can substantially lower your credit card payment just by calling them! I lowered my cable/internet bill by 75% just for calling! Get rid of the home telephone – you never use it anyway. Use cash envelopes for the categories you tend to spend impulsively (groceries, restaurants, shopping, entertainment, spending money). Call and get a new quote on your homeowner’s/auto insurance.

-

Chop up the credit cards!

If they are a crutch that keeps trapping you, it is time to chop them up. I chopped up my credit cards December 2002!

-

Make it a family effort!

There is NOTHING like a unified family. Nothing.

-

Pay secured debt before unsecured debt.

If you can’t pay everybody, consider paying just the secured debts. Call the unsecured companies and tell them that you will not be able to pay them this month, but that you fully intend to pay them. Tell the truth! There is power when you call someone and ask for help! They may or may not work with you, but when you are in bad shape financially you can’t pay them if you want to!

What are some other ways to fill in the “Go Get This” Gap?

Back to School?

School supplies? What does school even look like this year?

If you’re a parent, you are probably wondering what back-to-school will look like this year.

Maybe you are waiting for your school district to announce their plans for the year, or possibly the year’s start has already been delayed. Parents are trying to decide between a multitude of options – send the kids back to classrooms full time, hybrid schedules mixing in-person and online, eLearning through your school district, co-ops with other parents, or homeschooling.

There is a lot of uncertainty right now about what this school year will look like. So whatever you are gearing up for, we want to help.

Where do you start when it comes to scoring great deals on school supplies? Below is a list of tips and tricks for back-to-school shopping compiled by one of the I Was Broke. Now I’m Not. team members, Whitney Purcell, along with a few of our other moms. Whitney is a mom of two little girls (3 and 6) and has spent a great deal of time researching back-to-school deals.

When to Shop for School Supplies

Knowing when to shop can help you save a lot of money. We suggest checking to see if your state has a tax-free weekend and when retailers are planning to run specials.

Tax-Free Weekend

Shop during your state’s tax-free weekend is a great way to save money. You not only avoid paying sales tax on clothing and school supplies, but most retailers run specials that weekend as well.

Before you head out to do your shopping, do your research. Different states have different restrictions on what is tax-free. While most states include school supplies and clothing, you’ll want to check in advance. To see when your state’s tax-free weekend is and what it covers, click HERE.

If you are in a state that doesn’t offer a tax-free weekend, it could be worth driving to another state close by, especially if you need to purchase high priced items. Growing up in Kansas, we didn’t have a tax-free weekend, but Missouri was only a 30-minute drive, so going there to purchase back-to-school clothes and supplies was worth the trip.

This year some states, like Tennessee, are planning to have two tax-free weekends!

Store Specials

Another great time to shop is when a retailer is running specials. Check out stores like Target, Walmart, and office supply stores to see their specials. Typically this will start the beginning of August. Remember, you don’t have to purchase all of your supplies at one store – by shopping ahead of time, you can figure out where to buy what to save the most money.

You know Walgreens? Well, it isn’t just your drug store on every corner. Walgreens carries school supplies as well. While they aren’t the best priced, they offer great specials throughout the year, which includes deals on school supplies. Check out their weekly ads and coupons to see if school supplies are on there.

Where to Shop for School Supplies

You may feel like you are bombarded with options when it comes to where to shop. Don’t look past the unexpected locations, though.

First Get a Rebate

Before you use any of the store websites on our list, you should use Rakuten to get cashback your purchase. Once you sign up for a Rakuten account, you can add their browser app which will notify you when they have cashback for a participating retailer.

If you don’t like the browser extension, you can also go to their website before visiting an online store. For example, I just logged into my account, did a search for Target, and it came up with 1% cash back. I click on the Shop Now button and it takes me to Target’s website.

That’s it! Whatever I purchase I get 1% cash back. The amount of cashback varies greatly by store. I have seen as much as 22% cashback at some small retailers or on specific items, but it is usually around 2%-3%.

[su_button url=”https://www.josephsangl.com/go/rakuten?SID=school_supplies” rel=”sponsored” target=”blank” background=”#3E9369″ center=”yes” radius=”10″ size=”8″]Get Started with Rakuten[/su_button]

Target

Yes, I know this one may seem obvious, but I will be amiss if I didn’t mention it. Not only does Target offer great specials for back school, but it has wonderful clothing options for kids.

Did you know that their Cat & Jack line has a one year warranty? My daughter’s legging had a hole in them, so I took them back. I didn’t have a receipt, so they looked up the item number to verify when it was purchased and replaced them with no questions. Not only that, but they run wonderful specials for Black Friday each year, including summer clothes, so I stock up online and avoid the lines.

Bulleye’s Playground (formally the Dollar Spot) has great deals on classroom supplies. Some of these are geared more towards teachers this time of year, but that is great if you plan to homeschool or do eLearning. I’ve purchased pencils, workbooks, whiteboards, etc. for my kids there. They love being able to practice their letters and numbers using these inexpensive tools.

If your kids are going back to the classroom, this may be a great place to find gifts for your children’s teachers (and we all know they are deserve a great gift)! Remember, if you add a whole bunch of unnecessary items to your cart, you won’t be saving in the long run – something I have to remind myself of continually (with the help of my husband).

If your kids are going back to the classroom, this may be a great place to find gifts for your children’s teachers (and we all know they are deserve a great gift)! Remember, if you add a whole bunch of unnecessary items to your cart, you won’t be saving in the long run – something I have to remind myself of continually (with the help of my husband).

You can find Target’s weekly specials [HERE]. Deals vary by location, so make sure to check out the ads beforehand. At some locations they are offering Crayola markers and crayons for $0.99, kids scissors for $1.49, paint sets for $1.99, plastic folders for $0.50, and notebooks for $0.69. They also offer a 2-pack of kids’ fabric face masks for $4.

Aldi

I love Aldi! I love my low bill when I leave. I love the savings on my groceries. I also love their seasonal goods, including their school supplies this time of year.

Their weekly ads will show their specials, and when they expect to get items in stock. Aldi also gives you a sneak peek of what will be the next week’s specials so you can plan ahead. I suggest going on the first day the school supplies are stocked because these specialty items can sometimes sell out quickly. While some stores may restock, for some locations, once they are gone, that’s it.

Aldi is another excellent location for tissues and disinfecting wipes, which schools will most likely ask for in abundance this year.

I’ve also seen great deals on character backpacks, lunch boxes, insulated food containers, and kids reusable water bottles. They even have lunch storage containers with compartments for their entree and sides.

I’ve also seen great deals on character backpacks, lunch boxes, insulated food containers, and kids reusable water bottles. They even have lunch storage containers with compartments for their entree and sides.

If you need additional learning materials for at-home, Aldi offers educational puzzles and elementary age perforated page activity books. My daughter is working through their kindergarten book right now. They review letters, shapes, colors, and sight words. Aldi also had a summer review activity book this year.

Walmart

I’ll be the first to say that Walmart wasn’t my favorite place to shop. While they have low prices, our local Walmart always had long lines and not the best customer service.

However, when Walmart introduced its grocery pickup with a convenient app where I could do my grocery shopping in my sweatpants at home, I became a Walmart shopper.

Most moms will agree it is no fun running errands with kids in tow. In and out of the car seats in the heat – no, thank you! Getting Walmart’s low prices without standing in lines is a massive win in my book. Check out their back to school specials [HERE].

Dollar Stores

Check the Dollar Store, Family Dollar, or Dollar Tree for back-to-school items like basic calculators, planners, colored pencils, or clipboards. This will help you save money while still getting a great item. Most stores stock school supplies year-round, including name brand items at some.

Amazon

Amazon often has the lowest price on items, so make sure to check items against Amazon. I’ve found if you’re ordering multiple of an item (like glue, markers, etc.) they have better prices. It also saves you on spending extra money on gas running around town, especially if you’re already paying for Prime.

Amazon often has the lowest price on items, so make sure to check items against Amazon. I’ve found if you’re ordering multiple of an item (like glue, markers, etc.) they have better prices. It also saves you on spending extra money on gas running around town, especially if you’re already paying for Prime.

We’ve included an Amazon shopping list to help you get started, click HERE.

Office Supply Stores

Office supply stores can have a reputation for being a bit expensive. They offer such a wide range of products that their draw is they have everything you need, not that they are the most inexpensive. However, during back-to-school, they will run specials. I’ve seen sets of colored pencils on sale for half of what they are listed for at other retailers. Check out their ads. If you can pop in quickly for a few items while you’re running errands, it may be worth the trip.

Craft Stores

Check out stores like Michael’s, Hobby Lobby, or JOANN for school supplies.

BONUS – These stores usually have coupons that you can easily find online. I have the Michael’s and Hobby Lobby apps on my phone, so I can pull up their weekly coupon at checkout. If you don’t have the app, don’t worry about printing the coupons ahead on time, just make sure you have their website pulled up with the online coupon.

How to Shop for School Supplies

We’ve talked about when and where to shop, but it’s also important to consider how you shop. If you buy everything in one location and pay no attention to the sales, you leave savings on the table.

Order in Bulk

If you have multiple kids or have a friend who is willing to split supplies, look at ordering in bulk to save money. Some retailers (ex. Amazon) will have a multi-pack of paints, sets of markers, scissors, etc. that you can purchase. Purchasing in bulk will help save you money per set.

This also applies to items like Clorox wipes, sanitizer, and tissues. If you buy a multi-pack, you save per item, and you can keep the extra for your household stock.

Look at What You Already Have

If you’re like me, you love a good deal. So when I see something on clearance that I know we will need soon, I will scoop it up. Don’t forget to check if you already have it at home before you buy more.

If you’re like me, you love a good deal. So when I see something on clearance that I know we will need soon, I will scoop it up. Don’t forget to check if you already have it at home before you buy more.

Since kids were sent home early last year, chances are there are some unused items they can take this year. For instance, I have a few glue sticks that my daughter never used. Look through last year’s supplies for unused items that you can reuse this year.

Generic Brands

Don’t shy away from generic brands. There is a stigma that generic is inferior to name brands. However, that is not the case.

Some generic brands may not be a good deal over time if you have to replace them quicker or don’t work well. However, some stores (ex: Target) are making quality products (markers, colored pencils, etc.) that will save you money but still deliver the performance that your child needs.

Store Pickups and Online Shopping

Schedule store pickups for your school shopping. By utilizing curbside pick up options from Walmart, Target, Aldi, and more, you can save yourself time and money.

If you don’t have to go into each store, you are more likely to shop around and choose different stores for the best prices on individual items. You can add them to your current grocery pick up, so it doesn’t cost you an extra trip.

If you want to avoid the stores altogether, we’ve included an Amazon shopping list with some of our suggestions. No running around town – just click HERE and send!

Coupons

COUPONS! Couponing may not be your normal habit, but back-to-school is a great time to look for coupons that could save you money on supplies.

COUPONS! Couponing may not be your normal habit, but back-to-school is a great time to look for coupons that could save you money on supplies.

Check magazines, newspapers, or online coupon sites for options. On our budgeting page on the I Was Broke. Now I’m Not. website, we have links to several online coupon sites. This is a great place to start.

If a store has an app (like Michael’s or Hobby Lobby that I mentioned earlier), check it before shopping to see if they have any special deals. You can find great deals and look for in-store coupons. For instance, the Target app will show you their weekly specials, and you can add Target Circle Offers to save even more.

Loyalty Rewards

As you’ve been purchasing items, you’ve been earning rewards at a lot of stores throughout the year. Look to see what stores you’ve earned reward points and exchange your points for school supplies, clothes, or shoes.

You may want to check if you have credit card points to redeem. If so, choose a store where you’ll do back-to-school shopping and get a gift card there. We’ve redeemed our points for Walmart and Target gift cards.

Price Matching

Does a store that you’re shopping at offer price matching? Stores like Staples, Target, Kohl’s, Office Max, and Office Depot offer price matching. Check each store to learn about its policy and restrictions.

Happy School Supply Shopping

I know making decisions about school during COVID-19 has been difficult and stressful for parents and school officials alike. So, however, and whenever your kids return to school this fall, we hope you find this helpful. Remember, there is no “right way” for everyone, so give yourself and others grace! Happy (and thrifty) shopping!

How have you saved money back to school shopping?

5 Ways to Save Money Without Selling Anything

When the economy takes a down turn, one of the best ways to “weather the storm” is to save money! In this post I will share the top five ways that we see people saving lots of money.

I believe that if you apply these five items, you will save over $1,000 a year. Don’t believe me? Try them out!

1. Home and auto insurance

I know that I have mentioned this several times on the blog, but it is so true! I have had HUNDREDS of stories of people telling me about how much money they have saved by getting new quotes.

Many of them never had to change their current insurer because they took the better quotes back to their current insurer and demanded a better deal. Sweet!

On our Next Steps Insurance page we have links to get both Auto and Homeowner’s insurance quotes. These allow you to fill in a bit of information and receive quotes without the hassle of having to call around to multiple different companies.

Remember when LendingTree said “When banks compete, you win!”? Well, the same is true for insurance companies. Be sure to get your home/renter’s insurance quoted along with your auto insurance because bundling them together will save you 10% – 30%.

2. Life insurance

It is incredible the number of people who have dependents reliant upon their income yet do not have life insurance. According to LIMRA only 59% of Americans have life insurance, and have of those with insurance have inadequate coverage.

As a teacher and speaker on the subject of personal finances, I have seen many examples of inadequate/no life insurance. The impact that it has on the surviving dependents is devastating. I have also seen instances where there was adequate insurance. The result is much different!

I have also seen a lot of people who are paying way too much on life insurance. Some people are paying thousands of dollars a year in life insurance premiums who tell me that the cash value will be worth $1,000,000 when they retire. I tell them that this is great, but if they would have term life insurance and invest the difference in cost, they would have $10,000,000.

I recommend term life insurance equal to eight to ten times one’s annual take-home pay. For healthy people term life insurance is SO CHEAP. I personally carry thirty year level term policies on my bride and me.

You can obtain online quotes without speaking to anyone HERE

Go ahead and check them out. If you do not have life insurance and you have dependents who are reliant upon your income, purchase a policy ASAP. If you already have life insurance, compare the costs.

My bet is that you will save a ton of money.

3. Zero-percent balance transfer credit cards

I do not know how the credit card industry has been so effective at teaching Americans to believe that 15% is a good interest rate. But they are great at it! I cannot tell you the number of times I have heard the following statement during a financial counseling appointment:

“The interest isn’t bad on this card. It is only 17%.” Or 13%. Or 11.99%. Or … You get the picture.

I used to say the same thing (when I was BROKE). I got “unBROKE” by challenging my belief system and realized that I was allowing myself to be legally robbed of my money!

If you are paying high interest on a credit card, you should seek to restructure that debt. One great way to restructure debt is to play the “surf the balance” game. Move the balance to a zero-percent balance transfer credit card and then work like crazy to pay it off. If it is not paid off by the end of the zero-percent period, surf it again. This ensures that all of your payment goes to reduce the principal balance of the debt.

There are several 0% Balance Transfer Credit Cards located on the “Next Steps” tab (HERE). Move the balance and make progress toward 100% debt freedom!

You will save a ton of money by restructuring high interest debt!

4. Online savings accounts

Do you have money in your savings account? If not, it should by your TOP PRIORITY. $1,000 as a minimum or $2,500 if you have kids or a house. I repeat – this should be your TOP PRIORITY!

For those with money in savings, how much interest is your bank paying you? If it is a local bank, it is likely that the interest rate is very, very, very low (close to 0%). Online banks pay much higher interest because they do not have to pay the costs of maintaining local branches (people, buildings, etc). These online banks pay around 5X – 8X the national savings interest rates of other banks. I hold all of my savings in online banks and have done so since 2007. They are FDIC-insured and are very easy to use.

There are several excellent online banks. Click HERE to see the online banks I use or recommend.

The bottom line is that your money should make you money – the most money possible. My online banks allow me to do that for all money that I plan on using within the next five years.

5. Groceries and cash envelopes

Cash envelopes allow me to save a TON of money. How? I have a written spending plan that my bride and I prepare every month. In this written plan there are several items that I tend to be impulsive with. Groceries, dining out, clothing, entertainment, and spending money are the top five impulsive categories for me (can I get a witness?). To control my impulsiveness, we pull that money out in cash. We stow away the debit card and only allow cash to be used to purchase items in our impulsive categories.

This one move saved us over $200 a month in groceries alone! You can read more about how to start with cash envelopes HERE.

You can also use coupons to save a ton on groceries. In fact, my team has prepared an entire section of money saving tips for groceries under the Next Steps budgeting tab. You can check it out HERE.

Our Top 5 Ways to Save Money

Saving money, especially a large amount of money, can seem impossible. Our hope is that after reading this blog post you come away with practical ways to save money NOW!

Some of these savings ideas will take some work. No one ever says, “I’d love to be on the phone with different insurance companies all day!” However, if it means saving $500 or more each year those phone calls are worth it. Not to mention, most companies now offer online quotes that eliminate the hassle of waiting on hold. We’ve heard from numerous people that after they called for new quotes not only are the saving money, but they’re also getting better coverage.

Decide to take action today. Think about the last time you got a new insurance quote. If you have balances on credit cards look into transferring them over. Move your savings to an online bank to earn more interest and save on banking fees. Identify areas where you overspend, and start using cash envelopes and coupons for those things.

I believe that by pursuing these five money saving areas you can save $1,000 or more. Tell us how you did!

How Do I Stop Impulsive Spending?

Recently, I was teaching the Financial Learning Experience at my local church when I had a gentleman raise his hand and asked this question.

“How Do I Stop Being Impulsive?”

My answer? I don’t know to stop the impulsive nature, but I DO know how to control my impulse to spend recklessly.

I am a SPENDER. I am the type of person who would go out and accidentally buy a truck. I am a spender to my very core. I like buying things. You could say impulsive spending comes naturally to me. The best way I’ve found to combat my impulse to spend is being intentional about my finances.

Here are some steps I have taken that helped me reign in my impulsive spending nature, and it has allowed us to win financially!

A Written Spending Plan

The first thing that helped me reign in my impulse to spend is putting together a written spending plan EVERY month BEFORE the month begins. Jenn and I continue to do this EVERY month BEFORE the month begins. Did you catch that? EVERY month.

The first thing that helped me reign in my impulse to spend is putting together a written spending plan EVERY month BEFORE the month begins. Jenn and I continue to do this EVERY month BEFORE the month begins. Did you catch that? EVERY month.

It reinforces the fact that we cannot flippantly spend our money and expect to succeed. When you have personally helped prepare the spending of your money on paper, you are much more aware about whether or not you can afford the “I WANT THAT!” item.

Having a written plan means that each month you have already told your money where to go on paper before the month even starts. Instead of wondering, “Can I afford this?” or thinking “Maybe it will be okay just this once,” you already know the answer. You know what you have allocated for each category, and if you spend impulsively how it will break the budget.

Jenn and I use the budget forms that are available on the TOOLS page of our website. If you want more information about how to start budgeting check out our post “How Do I Budget?” for tips on how to get started. Trust me, the word budget doesn’t have to send chills up your spine. I can, and it will help you win with you money!

Cash Envelopes

Like I said before, I am an impulsive spender, but even I will not impulsively spend money on the electric bill. I won’t impulsively purchase gasoline. I don’t impulsively send extra money to the cable company. There are some things that I am not going to impulsively spend money on.

However, there are some things that I am VERY impulsive about. Items like groceries, dining out, clothes, spending money, and entertainment. I can go through some money really fast with these items! Since I know that I am impulsive for these spending categories, I use cash envelopes.

However, there are some things that I am VERY impulsive about. Items like groceries, dining out, clothes, spending money, and entertainment. I can go through some money really fast with these items! Since I know that I am impulsive for these spending categories, I use cash envelopes.

At the start of the month we add up the amount we have put in the budget for these categories. We then pull that amount out in CASH. The rule is that we can not pull more money out from the bank AND we can not use the ATM or debit card. I can not overspend cash.

To read more about why I LOVE cash envelopes check out this post.

Chop Up Credit Cards

You may pay yours off every month, but the vast majority of Americans do not. I was part of the vast majority, and I had to admit that I was a completely loser with credit cards. I ran those stupid things up three different times. I was stupid with them. They really catered to my impulsive nature. So I did what had to be done and applied the scissor blades to them and shut the accounts down.

You may pay yours off every month, but the vast majority of Americans do not. I was part of the vast majority, and I had to admit that I was a completely loser with credit cards. I ran those stupid things up three different times. I was stupid with them. They really catered to my impulsive nature. So I did what had to be done and applied the scissor blades to them and shut the accounts down.

After years of not using credit cards I do have them again now. How do I keep myself in check? Well, I still don’t use them on things I am impulsive about. Can I use them to pay utility bills? Yes! Can I use them to book travel for work trips? Yes! Do I use them for my spending money that I have budgeted for each month? Absolutely NOT!

Many of you are like me – you need to kill the bad spending habits, and the only way to do that is to get rid of the card. If you are able to have them later on you have to make sure you have accountability in place – like a budget that you review with your spouse or not using them for things you are tempted to overspend on.

How do I eliminate the credit card debt I already have from impulsive spending?

Maybe you are thinking, “Joe, that sounds great, but I’ve already wracked up credit card debt.” If you have questions about how to pay off credit card debt check out our post “You Can Be Debt-Free.” You can also listen to our Monday Money Tip podcast episode on “0% Balance Transfer Credit Cards” or check out options of 0% balance transfer credit cards on our Next Steps page to see if they can help you eliminate your credit card debt.

If you are a fellow spender, what have you done to control your impulsive spending habits?

Let there be…TIME

Sometimes the best cure for the “I wants” is time. The moment we see it we want it, however if we wait to purchase sometimes the desire fads.

If today you see the shiny new motorcycle your neighbor just bought you may think “I want one.” Don’t run down the street to your local dealership and purchase it right away. If you wait a few weeks it will bring clarity. “That motorcycle is awesome, however I really would rather save up for a boat that my whole family can enjoy.”

The more time between the “I WANT THAT!” moment and the actual “Purchasing Decision” moment, the clearer the decision will be. Impulsivity can lead to buyers remorse, and a slue of unnecessary things filling your home that you really don’t need (or want for that matter).

Seek Advice

One of the best ways to stop impulsive spending is to seek guidance from someone you trust and wants to see you prosper. I’ve said this before and I’ll say it again (and again and again), find wise financial counsel. If you are married include your spouse.

Having someone else invested in seeing you succeed financially creates accountability and will encourage you along the way. It’s a lot easier to stay the course, and stop the impulsive spending when you know you are going to have to answer for the purchases you’ve made.

Stay The Course

We are ALL impulsive. It seems to be different things for each of us, but we all have a case of impulsiveness every now and then.

If you do get off course – make the rash purchase – don’t let it derail you. Tomorrow is a new day, and a new opportunity to make wise spending choices. Look at what lead to your impulse purchase, and think about ways to prevent something like that in the future.

I wonder if any of you out there would share some “near misses” where you almost made a horrible, snap-judgment financial decision but you did not. What helped you make the decision to back out? How does it feel now as you look back on the situation?