Archive for December 2007

Save Money For Next Christmas – Part 4

In this series, we are learning how to ensure we pay cash for next Christmas!

Step 1 Determine how much money you want for Christmas next year

The goal in this step is to use the Mini-Budget Form (Excel) to determine the amount of money that you want for next year's Christmas.

Step 2 Save EVERY month for Christmas next year

By saving for Christmas every single month of the year, you can really lighten the financial burden that is regularly felt in November and December's budget!

By making your savings automatic, you help ensure that you stick to you savings plan!

Step 4 When Christmas shows up, pull your savings out in cash

You have done great! You have planned your spending and actually saved up the money! Now, it is Christmas time. There is one more hurdle to jump – sticking to your spending plan! I highly recommend that you use the cash envelope method. Why? Because when you spend cash, it is IMPOSSIBLE for you to spend more than you planned! It is the ultimate accountability! When you run out of cash, you are done!

I have found that when I spend cash, I am much more frugal and I usually end up getting a lot better deal than if I would have paid with a credit card. Why? I really can't explain it. I think it has to do with the fact that I am less impulsive and that means I think longer before making the purchase.

Well, that is it! That is how I have managed to pay cash for Christmas every single year starting in 2003. Here's to you having an all-cash, debt-free Christmas next year!

Enjoy this series? Consider subscribing for FREE to receive each post from www.JosephSangl.com in your E-MAIL.

Save Money For Next Christmas – Part 3

In this series, we are learning how to ensure we pay cash for next Christmas!

Step 1 Determine how much money you want for Christmas next year

The goal in this step is to use the Mini-Budget Form (Excel) to determine the amount of money that you want for next year’s Christmas.

Step 2 Save EVERY month for Christmas next year

By saving for Christmas every single month of the year, you can really lighten the financial burden that is regularly felt in November and December’s budget!

Step 3 Make it AUTOMATIC!

Anyone who has ever participated in a Christmas Club savings account KNOWS how great it is to have the savings be AUTOMATIC! When you make anything automatic, it helps you stick to it. If you automatically go to gym every morning, you will stay in shape. If you automatically read your newspaper every morning, you will stay informed. If you automatically SAVE, you will pay cash for Christmas!

One reason I regularly promote Capital One 360 Savings Accounts is because of their great interest rates with no minimum balance. Another reason is these accounts have a feature that allows you to AUTOMATICALLY draft your bank account at a set frequency. You can set it to draft your account monthly, weekly, bi-weekly, semi-monthly, or any other frequency you choose. You have determined the amount you need to save for next year’s Christmas. Now why not set up a bank account to keep you on course? If your bank pays competitive interest, you should contact them to have an automatic draft set up.

Save Money For Next Christmas – Part 2

This is the latest series brought to you by www.JosephSangl.com!

The goal of THIS SERIES is to equip you to pay CASH for next Christmas!

Step 1 Determine how much money you want for Christmas next year

The goal in this step is to use the [download#3#nohits] to determine the amount of money that you want for next year's Christmas.

Step 2 Save EVERY month for Christmas next year

You know the amount that you need for next Christmas! Congratulations! You have taken a HUGE first step toward being able to have a debt-free Christmas next year! Now, you need to save that amount! Jenn and I save 1/12th of our Christmas every single month. If our Christmas savings needs to be $1,000, we would save $83.33 every single month.

By saving every month, we really reduce the impact that Christmas has on our November and December budgets. In fact, it allows us to actually ENJOY spending money for Christmas because we are not worried about how we are going to pay off our credit cards!

Here is a chart to help you determine the amount to save each month.

Save Money For Next Christmas – Part 1

Welcome to the latest series brought to you by www.JosephSangl.com!

It is the day after Christmas, and you have just ran up a pile of debt on your credit cards again. It was fun to give great gifts, but it was not fun putting the purchases on the credit card.

If this is you, welcome to normal America. An America where we charge Christmas on credit cards, and attempt to use our tax refunds to help pay it back.

I remember when this was me. Each Christmas from 1992 to 2002 was a financially stressful time! I ran up a balance on the credit card and commit to use my tax refund to pay it back. The commitment was not very strong, however, because I always ended up carrying large balances on my credit card and paying high interest.

Since Christmas 2003, Jenn and I have paid CASH for all of our Christmas presents. Zero debt. No credit cards. No financial anxiety.

In this series, I will show you HOW we did it!

Step 1 Determine how much money you want for Christmas next year

Jenn and I always showed up a Christmas time without a plan. As a result, we overspent. Credit cards were always happy to catch our slack planning.

There is a great way to determine how much money you want for Christmas. You can pull up a [download#3#nohits] and list each person for whom you will purchase a present.

You might want to include line items like Christmas Cards, Postage, Christmas Tree, and "Unexpected Christmas Gift Needs".

The goal with this step is to obtain the amount you want for next Christmas. Is it $200? $500? $1,500? $5,000?

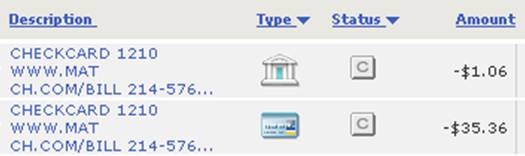

My VISA debit card number was stolen …

Last weekend, my lovely bride was Christmas shopping on-line. On Monday, I went to my bank's on-line site to make an on-line bill payment (I LOVE on-line bill payments!)

Here are some of the charges that I saw …

Now, I knew that she had been shopping on-line, but I didn't know that it was for a new spouse!!! Some of the fraudulent charges were from Match.com and Yahoo! Personals!

I called my bank, and they were fantastic! The person who used the card apparently used it as a credit card – they did not know my pin code. They immediately put a hold on the VISA check card and sent a new one to me. They have already reversed the charges and credited them back to my account.

So, I am now officially a fraud victim.

It makes me wonder how many www.JosephSangl.com readers have been a victim or know someone who has been a victim of this type of theft!

SUBSCRIBE to receive posts FREE via E-MAIL!